Discounted Materials Stock Picks

The materials industry is deeply cyclical with producers benefiting highly during an economic boom and many players going bankrupt in a bust. Hence an eye toward macroeconomic factors, such as demand for commodities, is necessary when investing in the materials sector. Grange Resources and Fortescue Metals Group are materials industry stocks on my list that are potentially undervalued, which means their current share prices are trading well-below what the companies are actually worth. Investors can determine how much a cyclical company is worth based on how much money they are expected to make in the future, or compared to the value of their peers. The list I’ve put together below are of stocks that compare favourably on all criteria, which potentially makes them good investments if you believe the price should eventually reflect the stock’s actual value.

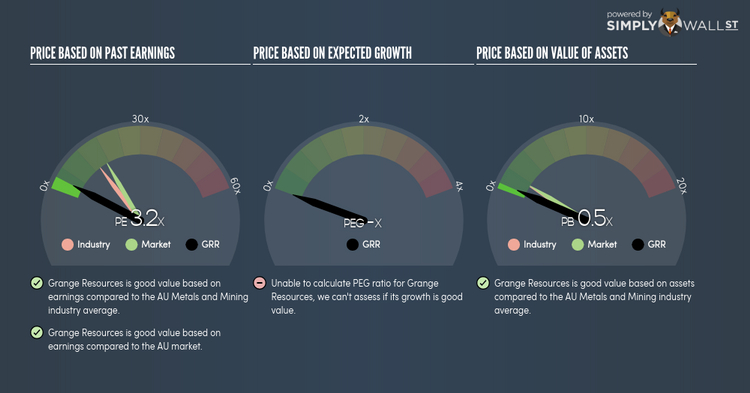

Grange Resources Limited (ASX:GRR)

Grange Resources Limited engages in the integrated iron ore mining and pellet production business in the northwest region of Tasmania. Grange Resources is run by CEO Honglin Zhao. The company currently has a market cap of AUD A$196.75M, putting it in the small-cap stocks category

GRR’s stock is now floating at around -25% under its true value of $0.23, at a price tag of AU$0.17, according to my discounted cash flow model. The difference between value and price signals a potential opportunity to buy GRR shares at a discount. What’s even more appeal is that GRR’s PE ratio is around 3.24x compared to its Metals and Mining peer level of, 14.01x implying that relative to its comparable set of companies, GRR’s shares can be purchased for a lower price. GRR is also strong in terms of its financial health, as short-term assets amply cover upcoming and long-term liabilities. Finally, its debt relative to equity is 1.25%, which has been reducing for the past few years signifying its capacity to reduce its debt obligations year on year. Continue research on Grange Resources here.

Fortescue Metals Group Limited (ASX:FMG)

Fortescue Metals Group Limited engages in the exploration, development, production, processing, and sale of iron ore in Australia, China, and internationally. Established in 2003, and headed by CEO Elizabeth Gaines, the company provides employment to 3,890 people and with the company’s market cap sitting at AUD A$13.48B, it falls under the large-cap group.

FMG’s stock is currently floating at around -38% less than its true value of $7.01, at a price of AU$4.33, based on its expected future cash flows. This mismatch signals an opportunity to buy FMG shares at a discount. In addition to this, FMG’s PE ratio is around 6.67x while its Metals and Mining peer level trades at, 14.01x indicating that relative to its peers, we can purchase FMG’s shares for cheaper. FMG is also robust in terms of financial health, with short-term assets covering liabilities in the near future as well as in the long run. The stock’s debt-to-equity ratio of 42.67% has been dropping for the last couple of years signalling FMG’s ability to reduce its debt obligations year on year. More detail on Fortescue Metals Group here.

South32 Limited (ASX:S32)

South32 Limited operates as a diversified metals and mining company primarily in Australia, Southern Africa, and South America. Formed in 2000, and now led by CEO Graham Kerr, the company currently employs 13,442 people and has a market cap of AUD A$16.58B, putting it in the large-cap category.

S32’s shares are currently floating at around -21% less than its actual level of $4.06, at a price tag of AU$3.22, based on my discounted cash flow model. This mismatch indicates a potential opportunity to buy low. What’s even more appeal is that S32’s PE ratio stands at 11.25x against its its Metals and Mining peer level of, 14.01x suggesting that relative to its comparable company group, you can purchase S32’s stock for a lower price right now. S32 is also a financially robust company, as current assets can cover liabilities in the near term and over the long run. Finally, its debt relative to equity is 10.25%, which has been declining for the last couple of years signalling its capability to reduce its debt obligations year on year. Dig deeper into South32 here.

For more financially sound, undervalued companies to add to your portfolio, explore this interactive list of undervalued stocks.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.