CEC International Holdings (HKG:759) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies CEC International Holdings Limited (HKG:759) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for CEC International Holdings

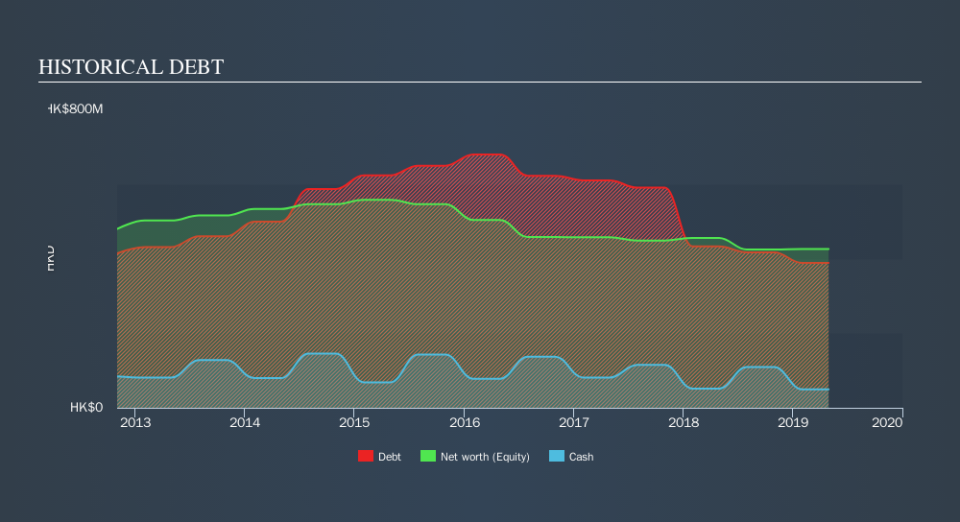

What Is CEC International Holdings's Debt?

You can click the graphic below for the historical numbers, but it shows that CEC International Holdings had HK$388.5m of debt in April 2019, down from HK$432.7m, one year before. However, because it has a cash reserve of HK$49.5m, its net debt is less, at about HK$339.0m.

How Strong Is CEC International Holdings's Balance Sheet?

According to the last reported balance sheet, CEC International Holdings had liabilities of HK$589.2m due within 12 months, and liabilities of HK$6.33m due beyond 12 months. Offsetting these obligations, it had cash of HK$49.5m as well as receivables valued at HK$21.2m due within 12 months. So its liabilities total HK$524.8m more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the HK$276.5m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt At the end of the day, CEC International Holdings would probably need a major re-capitalization if its creditors were to demand repayment.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

CEC International Holdings shareholders face the double whammy of a high net debt to EBITDA ratio (7.7), and fairly weak interest coverage, since EBIT is just 0.70 times the interest expense. This means we'd consider it to have a heavy debt load. One redeeming factor for CEC International Holdings is that it turned last year's EBIT loss into a gain of HK$14m, over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since CEC International Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Happily for any shareholders, CEC International Holdings actually produced more free cash flow than EBIT over the last year. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

To be frank both CEC International Holdings's interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. We're quite clear that we consider CEC International Holdings to be really rather risky, as a result of its balance sheet health. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. While CEC International Holdings didn't make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away.Click here to see if its earnings are heading in the right direction, over the medium term.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.