BAIC Motor (HKG:1958) Has A Somewhat Strained Balance Sheet

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, BAIC Motor Corporation Limited (HKG:1958) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for BAIC Motor

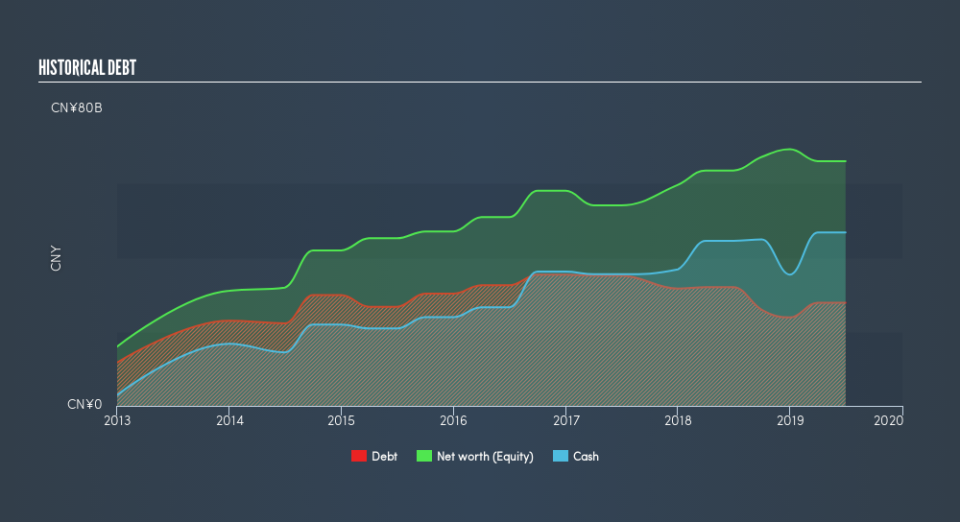

How Much Debt Does BAIC Motor Carry?

You can click the graphic below for the historical numbers, but it shows that BAIC Motor had CN¥27.8b of debt in June 2019, down from CN¥32.1b, one year before. However, its balance sheet shows it holds CN¥46.8b in cash, so it actually has CN¥19.0b net cash.

How Healthy Is BAIC Motor's Balance Sheet?

We can see from the most recent balance sheet that BAIC Motor had liabilities of CN¥105.5b falling due within a year, and liabilities of CN¥18.9b due beyond that. Offsetting these obligations, it had cash of CN¥46.8b as well as receivables valued at CN¥32.5b due within 12 months. So its liabilities total CN¥45.1b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of CN¥32.3b, we think shareholders really should watch BAIC Motor's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. Given that BAIC Motor has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

On the other hand, BAIC Motor saw its EBIT drop by 3.5% in the last twelve months. That sort of decline, if sustained, will obviously make debt harder to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if BAIC Motor can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. BAIC Motor may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, BAIC Motor produced sturdy free cash flow equating to 61% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

Although BAIC Motor's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of CN¥19b. So although we see some areas for improvement, we're not too worried about BAIC Motor's balance sheet. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check BAIC Motor's dividend history, without delay!

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.