Where Is Oil Going? You Won't Care if You Own These 3 Energy Stocks.

Oil prices are notoriously volatile. Over the past year, they have gone from a peak above $90 a barrel to a low point in the $60s. That volatility can have a significant impact on the earnings produced by oil companies.

However, some oil stocks are much less susceptible to the ebbs and flows of crude prices. Midstream giants Enterprise Products Partners (NYSE: EPD), Oneok (NYSE: OKE), and Enbridge (NYSE: ENB) stand out to a few Fool.com contributors for the overall stability of their earnings, since they don't have much direct commodity price exposure. You won't care too much about oil prices if you own these pipeline stocks.

Enterprise Products Partners generates cash through the cycle

Reuben Gregg Brewer (Enterprise Products Partners): Oil and natural gas prices rise and fall dramatically over time. But demand for these fuels, which are vital to the global energy system, tends to remain fairly robust regardless of energy prices. After all, people still need power even when economic activity is weak. That's why master limited partnership (MLP) Enterprise Products Partners is such a reliable income investment.

Enterprise owns the energy infrastructure that helps to move oil and natural gas from where it is produced to where it gets used. It largely gets paid for the use of its assets. The price of the commodities flowing through its system is far less important than demand for those commodities. The best example of how reliable Enterprise's business is? The 25 years of annual distribution increases it has provided to unitholders.

That streak is backed by an investment grade-rated balance sheet. And the MLP's distributable cash flow covered its distribution by a robust 1.7 times in 2023, leaving plenty of room for adversity before there's a risk of a distribution cut. To be fair, Enterprise's 7.1% distribution yield is going to make up the lion's share of returns here. But add in distribution growth of just 3%, which is pretty reasonable to expect in the future, and you've gotten to a 10% return. That's the kind of story both income investors and growth investors (perhaps reinvesting that big yield) could get behind.

Built to deliver resilient growth

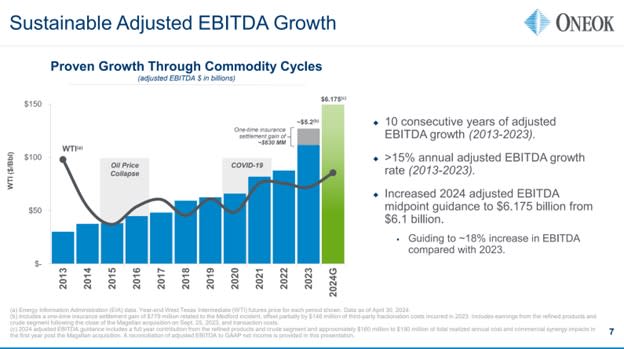

Matt DiLallo (Oneok): Oneok operates a diversified, integrated midstream system. The company owns 50,000 miles of natural gas, natural gas liquids, refined products, and crude oil pipelines. It also provides a variety of primarily fee-based midstream services to customers. These assets generate very stable cash flow based on the volumes flowing through its network, not the price of the underlying commodities. As long as energy demand grows, the company's earnings should keep rising, which has been the case over the past decade:

Oneok's durable business model has enabled it to deliver more than 25 years of dividend stability. While the pipeline company hasn't increased its payout every year, it has grown the dividend by more than 150% over the last decade, leading its closest peers.

The company is in a strong position to continue growing its earnings and dividends over the next four years. The primary catalyst is last year's $18.8 billion acquisition of Magellan Midstream Partners. That deal enhanced its diversification and growth profile. Oneok expects cost savings and commercial synergies to drive more than 20% free cash flow per share growth through 2027. The company recently sealed a smaller pipeline acquisition to accelerate its ability to capture those synergies.

Oneok expects its growing free cash flow to give it the fuel to increase its already attractive 4.9%-yielding dividend by 3% to 4% annually over the next four years. In addition, the company plans to repurchase $2 billion of its shares during that timeframe. It expects to deliver those cash returns while investing in organic growth projects and strengthening its already solid balance sheet.

So while oil prices might ebb and flow, Oneok should continue to grow its earnings, high-yielding dividend, and shareholder value in the coming years.

A reliable high-yield oil stock

Neha Chamaria (Enbridge): No oil and gas stock is immune to the fluctuations in oil and gas prices, but some can withstand commodity price shocks better than others, primarily because of their business model and capital efficiency. Enbridge is one such stock: If you own it, you needn't really worry about where oil is going, as the stock is likely to reward you in the long run regardless of how oil may have fared, thanks largely to its dividends.

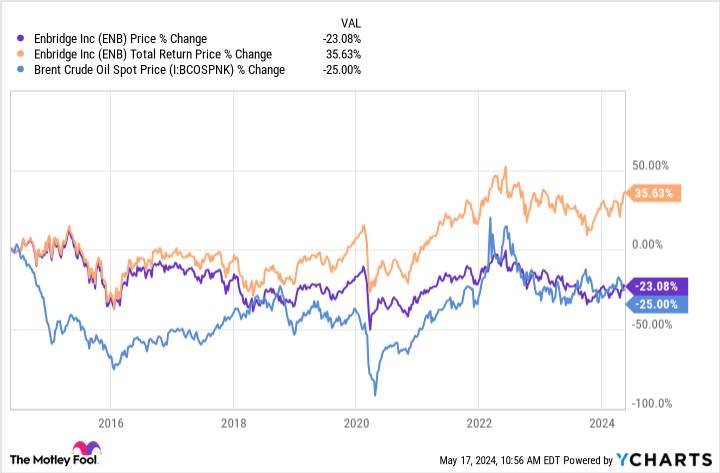

Enbridge has the largest liquids pipelines network in North America, transporting nearly 30% of all crude oil produced. It also moves large amounts of natural gas and has expansive gas distribution and storage facilities. These are regulated assets, and Enbridge provides its services under long-term contracts. In fact, as much as 97% of Enbridge's cash flows are underpinned by long-term contracts or toll settlements governed by the energy regulator. That makes its cash flows highly stable and predictable, which explains why Enbridge can afford to increase its dividend payout even amid falling oil prices. The energy infrastructure giant has increased its dividend every year for the past 29 consecutive years now and shareholders have reaped rich returns by reinvesting those dividends, as also evidenced in the chart.

Yet Enbridge plays it safe and pays out only around 60% to 70% of its distributable cash flows in dividends. That leaves the company with enough money to reinvest into its business and growth while ensuring its shareholders still receive bigger dividend checks every year. Overall, that makes Enbridge the kind of oil stock you can own at all times, with the stock's high dividend yield of 7.3% further adding to its appeal.

Should you invest $1,000 in Enterprise Products Partners right now?

Before you buy stock in Enterprise Products Partners, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enterprise Products Partners wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $566,624!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Matt DiLallo has positions in Enbridge and Enterprise Products Partners. Neha Chamaria has no position in any of the stocks mentioned. Reuben Gregg Brewer has positions in Enbridge. The Motley Fool has positions in and recommends Enbridge. The Motley Fool recommends Enterprise Products Partners and ONEOK. The Motley Fool has a disclosure policy.

Where Is Oil Going? You Won't Care if You Own These 3 Energy Stocks. was originally published by The Motley Fool