The three-year earnings decline has likely contributed toDP Eurasia's (LON:DPEU) shareholders losses of 27% over that period

As an investor its worth striving to ensure your overall portfolio beats the market average. But if you try your hand at stock picking, your risk returning less than the market. Unfortunately, that's been the case for longer term DP Eurasia N.V. (LON:DPEU) shareholders, since the share price is down 27% in the last three years, falling well short of the market return of around 19%. The last week also saw the share price slip down another 20%.

Since DP Eurasia has shed ₺25m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

View our latest analysis for DP Eurasia

Because DP Eurasia made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually expect strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

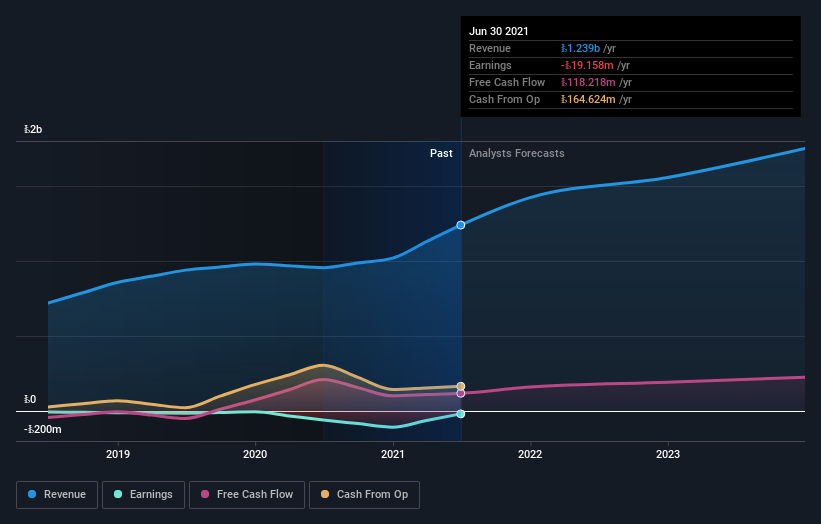

In the last three years, DP Eurasia saw its revenue grow by 13% per year, compound. That's a pretty good rate of top-line growth. Shareholders have seen the share price fall at 8% per year, for three years. So the market has definitely lost some love for the stock. With revenue growing at a solid clip, now might be the time to focus on the possibility that it will have a brighter future.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

This free interactive report on DP Eurasia's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

DP Eurasia produced a TSR of 1.6% over the last year. It's always nice to make money but this return falls short of the market return which was about 9.3% for the year. On the bright side, that's certainly better than the yearly loss of about 8% endured over the last three years, implying that the company is doing better recently. We hope the turnaround in fortunes continues. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Case in point: We've spotted 3 warning signs for DP Eurasia you should be aware of, and 2 of them make us uncomfortable.

We will like DP Eurasia better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.