Not Many Are Piling Into CRG Incorporated Berhad (KLSE:CRG) Just Yet

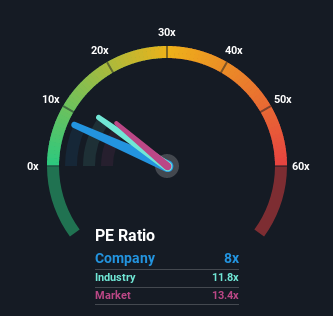

With a price-to-earnings (or "P/E") ratio of 8x CRG Incorporated Berhad (KLSE:CRG) may be sending bullish signals at the moment, given that almost half of all companies in Malaysia have P/E ratios greater than 14x and even P/E's higher than 24x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's exceedingly strong of late, CRG Berhad has been doing very well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

View our latest analysis for CRG Berhad

Although there are no analyst estimates available for CRG Berhad, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like CRG Berhad's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 458% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 412% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 12% shows it's noticeably more attractive on an annualised basis.

With this information, we find it odd that CRG Berhad is trading at a P/E lower than the market. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

What We Can Learn From CRG Berhad's P/E?

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of CRG Berhad revealed its three-year earnings trends aren't contributing to its P/E anywhere near as much as we would have predicted, given they look better than current market expectations. There could be some major unobserved threats to earnings preventing the P/E ratio from matching this positive performance. It appears many are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with CRG Berhad, and understanding these should be part of your investment process.

Of course, you might also be able to find a better stock than CRG Berhad. So you may wish to see this free collection of other companies that sit on P/E's below 20x and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here