Should Investors Buy the Recent Dip in Tesla (TSLA) Stock?

Tesla TSLA shares saw a nice rally Thursday after better than expected CPI numbers gave the broader market a nice boost. TSLA stock recently hit a new 52-week low of $177.12 per share as Elon Musk liquidated more Tesla shares following his Twitter acquisition.

With TSLA 52% from its highs, investors may be contemplating adding Tesla shares to their portfolio. Let’s take a look at the company’s outlook and valuation to see if it is indeed a good time to buy TSLA.

Recent Performance

Tesla reported its Q3 earnings last month and beat EPS expectations by 10% at $1.05 per share. The stock dropped despite the beat on the company’s bottom line. Top line growth was underwhelming, with sales missing expectations by 4% on revenue of $21.45 billion. Despite a record 343,830 deliveries during the quarter this slightly missed expectations as well.

TSLA stock is down -46% YTD to underperform the S&P 500’s -22%. Tesla shares are still up 721% over the last three years to crush the benchmark and its peer group’s +7%.

However, the company’s outlook is becoming more important with investors coming away less impressed with Tesla’s growth following its Q3 release. Tesla shares are still roughly down 14% since the report, even with its bounce Thursday.

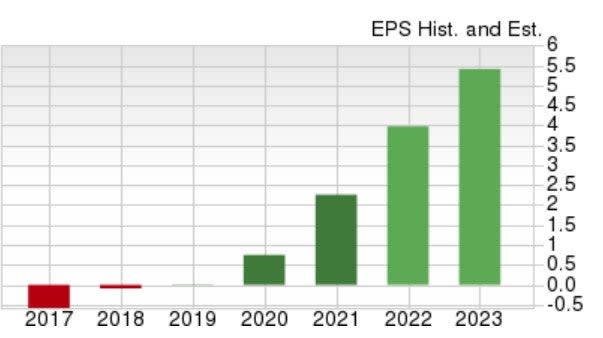

Image Source: Zacks Investment Research

Outlook

Year over year, TSLA earnings are now expected to rise 79% to $4.05. Fiscal year 2023 earnings are expected to rise another 30% at $5.29 per share. Top line growth is expected as well, with sales set to climb 54% this year and another 39% in FY23 at $115.38 billion. This is more than quadruple pre-pandemic sales of $24.57 billion in 2019.

Image Source: Zacks Investment Research

Earnings estimate revisions for this year and FY23 have trended up over the last 90 days. Rising estimate revisions are a good sign, especially with investors concerned over the premium paid for TSLA shares following its Q3 report.

Premium & Valuation

Trading around $190 per share, TSLA has a P/E of 43.8X. This is well above the industry average of 12.2X, which is where the premium may be a factor. However, Tesla remains the industry leader in the EV market and trades much lower than its decade high of 45,336X and the median of 236.9X. Also, industry peers like General Motors GM and Ford F are at far different stages of corporate life and aren’t experiencing growth like TSLA.

Image Source: Zacks Investment Research

Tesla’s price to sales is becoming more reasonable again as shown in the chart above. TSLA’s P/S of 8.2X is much lower than its decade high of 31.3X and near the median of 7.9X.

Bottom Line

TSLA still lands a Zacks Rank #3 (Hold) with its Automotive-Domestic Industry now in the top 27% of over 250 Zacks Industries. While there could be better buying opportunities ahead, Tesla continues to trade at a far better valuation than it has in the past. Also, electric vehicles are still a relatively small part of the auto industry market and the space still has massive potential to grow.

TSLA still appears poised for growth and earnings estimate revisions are up from last quarter. Patient investors could be rewarded for holding the stock with the average Zacks Price Target suggesting 66% upside from current levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tesla, Inc. (TSLA) : Free Stock Analysis Report

Ford Motor Company (F) : Free Stock Analysis Report

General Motors Company (GM) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research