Is XMH Holdings Ltd’s (SGX:BQF) Balance Sheet Strong Enough To Weather A Storm?

XMH Holdings Ltd (SGX:BQF) is a small-cap stock with a market capitalization of SGD27.82M. While investors primarily focus on the growth potential and competitive landscape of the small-cap companies, they end up ignoring a key aspect, which could be the biggest threat to its existence: its financial health. Why is it important? Given that BQF is not presently profitable, it’s crucial to understand the current state of its operations and pathway to profitability. I believe these basic checks tell most of the story you need to know. Nevertheless, since I only look at basic financial figures, I’d encourage you to dig deeper yourself into BQF here.

Does BQF generate an acceptable amount of cash through operations?

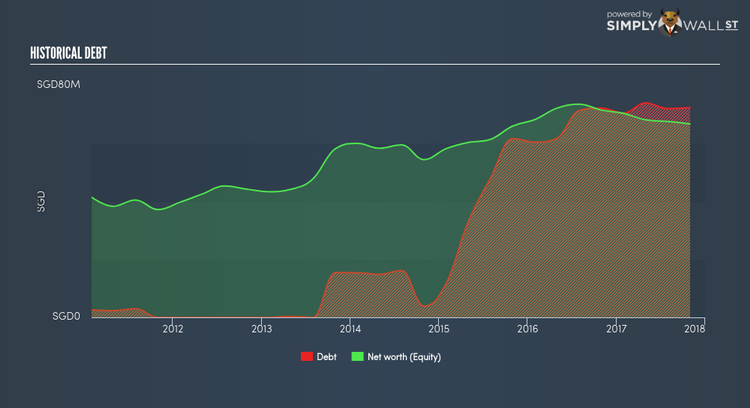

Over the past year, BQF has ramped up its debt from SGD61.8M to SGD74.0M – this includes both the current and long-term debt. With this increase in debt, BQF’s cash and short-term investments stands at SGD25.7M for investing into the business. On top of this, BQF has produced cash from operations of SGD2.6M during the same period of time, resulting in an operating cash to total debt ratio of 3.51%, indicating that BQF’s debt is not appropriately covered by operating cash. This ratio can also be interpreted as a measure of efficiency for loss making businesses as traditional metrics such as return on asset (ROA) requires positive earnings. In BQF’s case, it is able to generate 0.04x cash from its debt capital.

Does BQF’s liquid assets cover its short-term commitments?

Looking at BQF’s most recent SGD65.6M liabilities, the company has been able to meet these obligations given the level of current assets of SGD90.5M, with a current ratio of 1.38x. Generally, for trade distributors companies, this is a reasonable ratio as there’s enough of a cash buffer without holding too capital in low return investments.

Does BQF face the risk of succumbing to its debt-load?

Since total debt levels have outpaced equities, BQF is a highly leveraged company. This is not unusual for small-caps as debt tends to be a cheaper and faster source of funding for some businesses. But since BQF is currently unprofitable, sustainability of its current state of operations becomes a concern. Maintaining a high level of debt, while revenues are still below costs, can be dangerous as liquidity tends to dry up in unexpected downturns.

Next Steps:

Are you a shareholder? BQF’s cash flow coverage indicates it could improve its operating efficiency in order to meet demand for debt repayments should unforeseen events arise. However, its high liquidity means the company should continue to operate smoothly in the case of adverse events. Given that BQF’s financial situation may change. I suggest keeping abreast of market expectations for BQF’s future growth on our free analysis platform.

Are you a potential investor? With a high level of debt on its balance sheet, BQF could still be in a financially strong position if its cash flow also stacked up. However, this isn’t the case, and there’s room for BQF to increase its operational efficiency. However, the company exhibits an ability to meet its near term obligations should an adverse event occur. I encourage you to continue your research by taking a look at BQF’s past performance analysis on our free platform to figure out BQF’s financial health position.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.