Is TK Group (Holdings) (HKG:2283) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that TK Group (Holdings) Limited (HKG:2283) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for TK Group (Holdings)

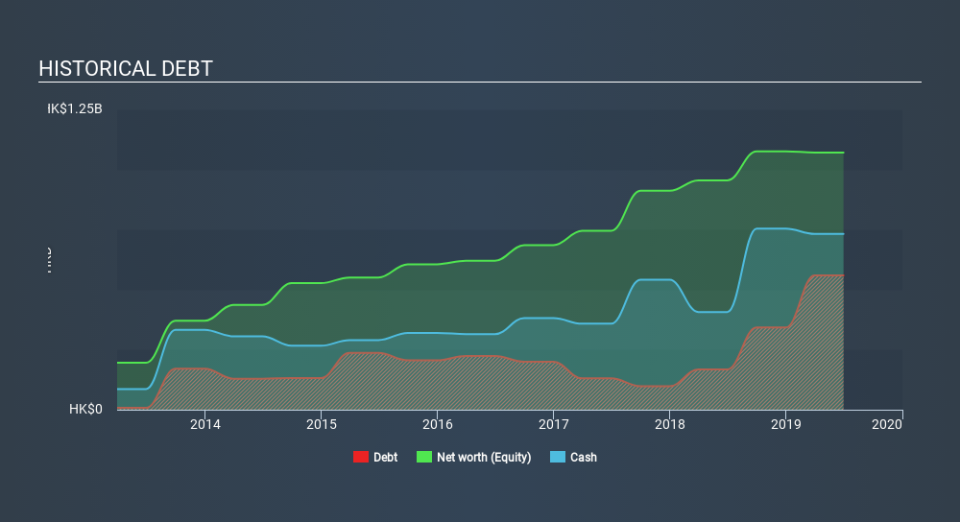

What Is TK Group (Holdings)'s Net Debt?

As you can see below, at the end of June 2019, TK Group (Holdings) had HK$559.3m of debt, up from HK$167.5m a year ago. Click the image for more detail. However, it does have HK$731.8m in cash offsetting this, leading to net cash of HK$172.5m.

How Strong Is TK Group (Holdings)'s Balance Sheet?

The latest balance sheet data shows that TK Group (Holdings) had liabilities of HK$842.3m due within a year, and liabilities of HK$578.4m falling due after that. Offsetting these obligations, it had cash of HK$731.8m as well as receivables valued at HK$325.3m due within 12 months. So it has liabilities totalling HK$363.6m more than its cash and near-term receivables, combined.

Since publicly traded TK Group (Holdings) shares are worth a total of HK$3.18b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, TK Group (Holdings) also has more cash than debt, so we're pretty confident it can manage its debt safely.

But the other side of the story is that TK Group (Holdings) saw its EBIT decline by 5.3% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine TK Group (Holdings)'s ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. TK Group (Holdings) may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, TK Group (Holdings) recorded free cash flow worth 54% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

Although TK Group (Holdings)'s balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of HK$172.5m. So we are not troubled with TK Group (Holdings)'s debt use. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for TK Group (Holdings) that you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.