Is It Time to Buy the Dip on Taiwan Semiconductor?

When companies take a tumble after an earnings report, it allows investors to assess whether the issue is a short-term problem or a long-term hurdle. If you have a long-term mindset, you can use short-term pessimism to your advantage and make some fantastic investments at a slightly lower price by going against the grain.

Taiwan Semiconductor (NYSE: TSM) recently reported its first-quarter results, which were met with a 6% sell-off during the trading day after they became available. While this wasn't as violent a sell-off as some companies experience, it's still noteworthy and could give investors a chance to get in on a stock that has seen its price rise substantially thanks to its involvement with artificial intelligence (AI) chips.

TSMC's new products will be in huge demand

Taiwan Semiconductor (TSMC for short) is the world's largest contract chip manufacturer. This means it doesn't make its chips to compete against other chipmakers. Instead, it uses its facilities to produce chips for companies like Apple and Nvidia, which design their own chips but don't have the equipment to manufacture them.

TSMC is a leader in chip technology and currently has industry-leading 3-nanometer wafers available. This measurement describes the distance between electrical traces on a chip, so the smaller the number, the more transistors it can pack onto a given chip. Although 3nm chips are the best technology available, the company's 2nm chip is scheduled for production starting in 2025.

When making a chip smaller, you have two options: Make it more powerful or more efficient. If a chip consumes less power to produce the same results, it saves in long-term operating costs, which is highly valued by clients that build a supercomputer slated for AI use that has millions of TSMC chips in it.

So the 2nm chip could drive another wave of demand, which would be a long-term boost for the company. In fact, management sees AI-related chips having a 50% compound annual growth rate (CAGR) for the next five years, which will shift its revenue mix to be greater than 20% in AI chips.

That's huge news as a drop in a different industry is currently hurting Taiwan Semiconductor.

Smartphones are to blame for TSMC's struggles

In 2023, TSMC's largest customer accounted for 25% of total revenue. While that customer isn't named in the first-quarter report, it's widely assumed to be Apple. In the first quarter, revenue from TSMC's smartphone division fell 16% year over year. This is a problem as smartphone revenue currently makes up around 38% of its total.

So, Taiwan Semiconductor is a tale of two divisions: the struggles in its smartphone segment, and what management calls the "insatiable" demand for its AI chips.

If you're a long-term investor, you're probably aware that the smartphone upgrade cycle is lengthening, which will be a long-term headwind for TSMC, although this could be near its peak now. However, the rise in AI chip demand is offsetting the new normal for the smartphone business.

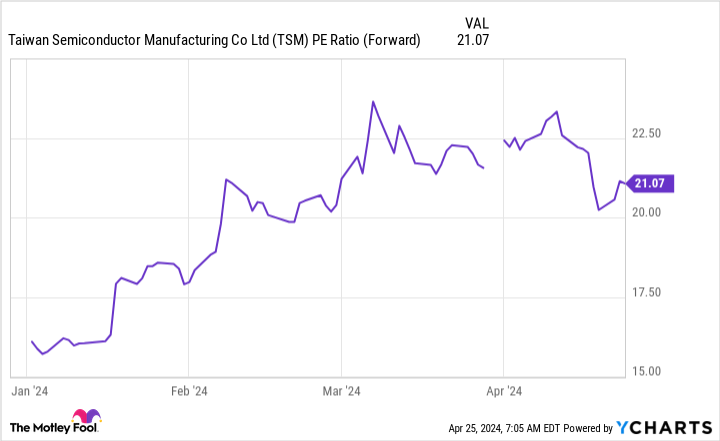

As a result, I think Taiwan Semiconductor will be just fine over the long term although it could take some time for the rest of the market to realize that. But because of the stock's decline, you can purchase shares in one of the most vital companies in the world for just 21 times forward earnings.

Compared to the S&P 500, which trades at 20.7 times forward earnings, I'd say Taiwan Semiconductor is a great value at this price.

So, with the slight sell-off thanks to some short-term worries, I think Taiwan Semiconductor is a great candidate to buy on the dip. But the dip wasn't very deep, so investors might consider moving quickly to take advantage of the cheaper price.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $529,390!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 30, 2024

Keithen Drury has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Is It Time to Buy the Dip on Taiwan Semiconductor? was originally published by The Motley Fool