What Investors Should Know About TC Orient Lighting Holdings Limited’s (HKG:515) Financial Strength

Investors are always looking for growth in small-cap stocks like TC Orient Lighting Holdings Limited (SEHK:515), with a market cap of HK$315.07M. However, an important fact which most ignore is: how financially healthy is the business? Companies operating in the electronic industry, especially ones that are currently loss-making, are inclined towards being higher risk. Evaluating financial health as part of your investment thesis is essential. I believe these basic checks tell most of the story you need to know. Nevertheless, this commentary is still very high-level, so I suggest you dig deeper yourself into 515 here.

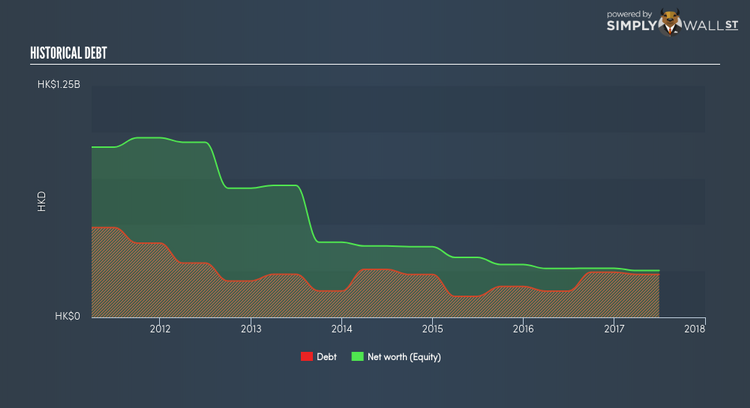

How does 515’s operating cash flow stack up against its debt?

Over the past year, 515 has ramped up its debt from HK$166.4M to HK$243.6M , which is mainly comprised of near term debt. With this growth in debt, 515 currently has HK$67.8M remaining in cash and short-term investments for investing into the business. However, its trivial cash flows from operations make the cash-to-debt ratio less useful to us, though these low levels of cash means that operational efficiency is worth a look. For this article’s sake, I won’t be looking at this today, but you can examine some of 515’s operating efficiency ratios such as ROA here.

Does 515’s liquid assets cover its short-term commitments?

At the current liabilities level of HK$642.0M liabilities, it appears that the company has not maintained a sufficient level of current assets to meet its obligations, with the current ratio last standing at 0.99x, which is below the prudent industry ratio of 3x.

Is 515’s level of debt at an acceptable level?

With debt reaching 91.55% of equity, 515 may be thought of as relatively highly levered. This is not unusual for small-caps as debt tends to be a cheaper and faster source of funding for some businesses. However, since 515 is currently unprofitable, there’s a question of sustainability of its current operations. Running high debt, while not yet making money, can be risky in unexpected downturns as liquidity may dry up, making it hard to operate.

Next Steps:

Are you a shareholder? 515’s high debt levels is not met with high cash flow coverage. This leaves room for improvement in terms of debt management and operational efficiency. In addition to this, the company may struggle to meet its near term liabilities should an adverse event occur. Going forward, its financial position may change. I recommend keeping abreast of market expectations for 515’s future growth on our free analysis platform.

Are you a potential investor? 515’s large debt ratio along with poor cash coverage in addition to low liquidity coverage of near-term expenses may not build the strongest investment case. But, keep in mind that this is a point-in-time analysis, and today’s performance may not be representative of 515’s track record. As a following step, you should take a look at 515’s past performance analysis on our free platform to conclude on 515’s financial health.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.