1 Glorious Growth Stock Down 49% to Buy Hand Over Fist, According to Wall Street

Many investors look to the Nasdaq Composite index to measure the performance of the technology sector. It set a new record high in the early stages of 2024 and remains comfortably in bull market territory despite a recent sell-off.

However, indexes like the Nasdaq Composite are heavily weighted toward multitrillion-dollar tech giants like Microsoft and Nvidia, which skews their performance. Many stocks at the smaller end of the technology industry are still trading below their best-ever levels as they grapple with challenging economic conditions, a scenario that presents an opportunity for long-term investors.

Workiva (NYSE: WK) offers a unique portfolio of software products designed to help organizations compile data and create essential reports. Its stock is trading 49% below its all-time high, yet most Wall Street analysts tracked by The Wall Street Journal have assigned it the highest possible buy rating. Here's why investors might want to follow their lead.

Simplifying the complex digital world

Almost every business process you can think of can now be handled digitally thanks to technologies like cloud computing. However, this means organizations are using dozens, or even hundreds of online applications to run their day-to-day operations, which can be a nightmare for managers tasked with tracking workflows.

Workiva's platform solves that problem. It's a cloud-based dashboard designed to aggregate data into one place by plugging into almost every major productivity application, file storage application, and system of record. It means managers no longer have to chase down data in each piece of software, which is critical in fragmented situations where some employees use Microsoft Excel and others might be using Salesforce.

Workiva goes one step further by offering hundreds of ready-made templates so that once data is neatly aggregated in one place, managers can rapidly compile reports for their executive team, or for regulators like the Securities and Exchange Commission. This is especially useful for publicly traded companies because they have stringent reporting requirements.

But Workiva is focusing heavily on another one of its solutions, which is specifically designed for environmental, social, and governance (ESG) reporting. Global governments are pushing companies to track the impacts of their operations beyond their financial results to help solve issues like climate change and equality in the workplace.

Workiva offers pre-built ESG frameworks, and it helps businesses create strategies and collect the necessary data to fulfill them. From there, they can easily compile reports for both internal and external stakeholders, which will be increasingly useful over time as regulators introduce more guidelines that require mandatory reporting.

Steady growth led by high-spending customers

Workiva just reported its financial results for the first quarter of 2024. The company delivered $175.7 million in revenue, equaling 17% growth compared to Q1 2023. It marked an acceleration both sequentially and year over year, suggesting the expansion in its product portfolio to include solutions like ESG reporting, combined with an improving economic climate, is bearing fruit.

The result was especially impressive considering Workiva actually shrank its operating expenses by 3.8% during the quarter, which would normally lead to slower growth. More revenue coming in with less money flowing out led to a net loss of just $11.7 million, which was a 74.7% reduction from the year-ago period when the company lost $46.1 million.

On a non-GAAP basis (which strips out one-off and non-cash expenses like stock-based compensation), Workiva eked out a profit of $12.6 million, which was a positive swing from its $6.6 million net loss a year ago.

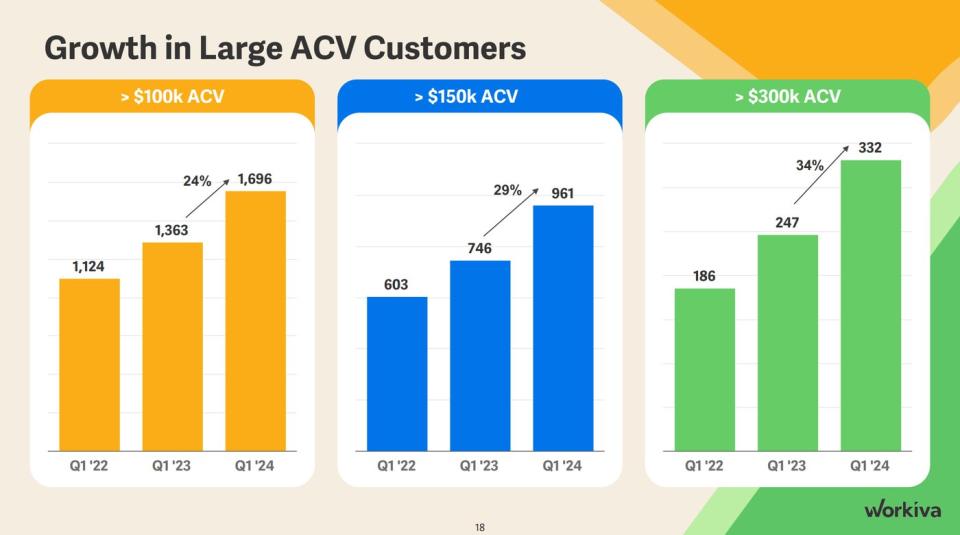

Workiva's strong Q1 results were underpinned by powerful growth among its highest-spending customer cohorts. The company serves 6,074 businesses worldwide, which was a modest 5.5% increase year over year, but the cohort spending at least $300,000 annually on its software grew by 34%:

Wall Street is bullish on Workiva stock

Workiva values its global addressable market at $25 billion across accounting and finance, compliance, and ESG reporting. ESG is still in its infancy right now, but it could grow to become the company's biggest opportunity. Governments around the world are gradually introducing new rules each year to force businesses into tracking their environmental and social footprints, and that will require the holistic reporting solutions Workiva provides.

Workiva stock is down 49% from its all-time high set during the tech frenzy in 2021. Its valuation was a little irrational back then, but the company has done nothing but grow and expand ever since, which makes it look like an attractive buying opportunity today.

Plus, the dip hasn't deterred Wall Street. The Wall Street Journal tracks 11 analysts covering the stock, and eight of them have given it the highest possible buy rating. As for the remainder, one is in the overweight (bullish) camp, while two recommend holding, and no analysts recommend selling.

The analysts have an average price target of $105.76, which implies an upside of nearly 30% from where the stock trades today. If Workiva's revenue growth continues to accelerate while it marches toward profitability, it probably won't take very long to get there.

Should you invest $1,000 in Workiva right now?

Before you buy stock in Workiva, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Workiva wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $544,015!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Microsoft, Nvidia, Salesforce, and Workiva. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

1 Glorious Growth Stock Down 49% to Buy Hand Over Fist, According to Wall Street was originally published by The Motley Fool