TSX Growth Leaders With High Insider Stakes In Canada

As Canadian markets continue to navigate through fluctuating economic conditions, investors are keenly observing trends and strategic opportunities. High insider ownership in growth companies on the TSX is particularly noteworthy, as it often signals strong confidence from those who know the company best. In this context, understanding the potential benefits of investing in such firms can provide a solid foundation for making informed decisions in an ever-evolving market landscape.

Top 10 Growth Companies With High Insider Ownership In Canada

Name | Insider Ownership | Earnings Growth |

goeasy (TSX:GSY) | 21.7% | 15.9% |

Payfare (TSX:PAY) | 15% | 57.7% |

Aritzia (TSX:ATZ) | 19.1% | 51.2% |

Allied Gold (TSX:AAUC) | 22.5% | 68.2% |

ROK Resources (TSXV:ROK) | 16.6% | 159.6% |

Aya Gold & Silver (TSX:AYA) | 10.2% | 51.6% |

Silver X Mining (TSXV:AGX) | 14.2% | 144.2% |

Ivanhoe Mines (TSX:IVN) | 13.2% | 65.3% |

Artemis Gold (TSXV:ARTG) | 31.8% | 38.7% |

Almonty Industries (TSX:AII) | 12.4% | 82.1% |

Let's dive into some prime choices out of from the screener.

Green Thumb Industries

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Green Thumb Industries Inc. operates in the United States, focusing on the manufacturing, distribution, marketing, and sale of cannabis products for both medical and adult use, with a market capitalization of CA$3.78 billion.

Operations: The company generates revenue primarily through its retail and consumer packaged goods segments, totaling $806.38 million and $583.78 million respectively.

Insider Ownership: 10.9%

Revenue Growth Forecast: 10.3% p.a.

Green Thumb Industries, a growth-oriented company with significant insider ownership, has recently shown robust financial performance. For Q1 2024, the firm reported a substantial increase in sales to US$275.81 million and net income to US$31.08 million. Despite trading at 38.5% below its estimated fair value and having low forecasted Return on Equity at 7.5%, GTII is experiencing notable earnings growth, projected at 23.55% annually over the next three years, outpacing the Canadian market's average. Additionally, recent expansions include opening new dispensaries and enhancing product lines in strategic locations like Florida.

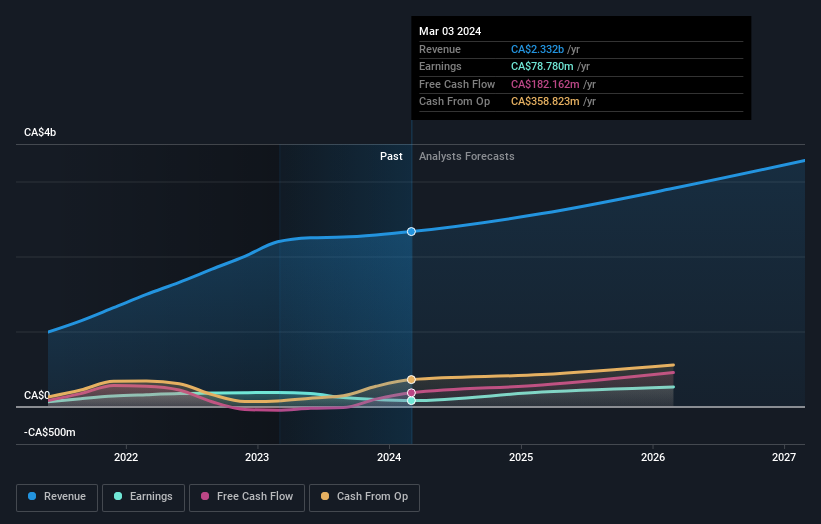

Aritzia

Simply Wall St Growth Rating: ★★★★★☆

Overview: Aritzia Inc. operates as a fashion retailer specializing in women's apparel and accessories, primarily in the United States and Canada, with a market capitalization of approximately CA$3.86 billion.

Operations: The company generates its revenue primarily from the sale of women's apparel, totaling CA$2.33 billion.

Insider Ownership: 19.1%

Revenue Growth Forecast: 11% p.a.

Aritzia, a Canadian retailer, is poised for substantial growth with earnings expected to surge by 51.2% annually, outstripping the market's forecast of 14.5%. Despite recent challenges reflected in a profit decline from CAD 187.59 million to CAD 78.78 million last year and a net profit margin drop to 3.4%, the company is trading significantly below its estimated fair value and analysts predict a price increase of approximately 24.4%. Revenue forecasts remain optimistic with an anticipated increase up to CAD 2.62 billion for fiscal 2025, alongside strategic share buybacks enhancing shareholder value.

goeasy

Simply Wall St Growth Rating: ★★★★★☆

Overview: goeasy Ltd. operates in Canada, offering non-prime leasing and lending services through its easyhome, easyfinancial, and LendCare brands with a market cap of approximately CA$3.12 billion.

Operations: The company generates revenue through its easyhome and easyfinancial segments, totaling CA$153.99 million and CA$1.17 billion respectively.

Insider Ownership: 21.7%

Revenue Growth Forecast: 32.7% p.a.

goeasy, a Canadian financial services company, has shown robust growth with a 54.3% increase in earnings over the past year and is projected to expand revenues by 32.7% annually. Despite trading 41.4% below its estimated fair value, concerns linger as its dividend coverage by cash flows remains weak. The recent appointment of Patrick Ens as President of easyfinancial and easyhome could strengthen leadership amidst these mixed financial nuances, potentially steering the company towards sustained profitability and operational efficiency.

Dive into the specifics of goeasy here with our thorough growth forecast report.

Our valuation report unveils the possibility goeasy's shares may be trading at a discount.

Key Takeaways

Unlock more gems! Our Fast Growing TSX Companies With High Insider Ownership screener has unearthed 28 more companies for you to explore.Click here to unveil our expertly curated list of 31 Fast Growing TSX Companies With High Insider Ownership.

Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include CNSX:GTII TSX:ATZ and TSX:GSY.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com