SMH ETF: Selloff Could Present Opportunity for Long-Term Investors

After a dazzling start to 2024, the VanEck Semiconductor ETF (SMH) has dropped 24.1% from its 52-week high and suffered a nearly 10% loss in the past week alone. However, for long-term investors, the selloff could present a long-term buying opportunity.

I’m bullish on the largest and most liquid semiconductor ETF due to its robust long-term track record, consistently outperforming the broader market over the past three, five, and 10 years. I’m also bullish on SMH and the semiconductor industry in general, given the strong long-term demand for semiconductors, which remains promising despite the sector’s recent decline.

Additionally, many of the top semiconductor stocks in SMH’s portfolio don’t look particularly expensive after the recent selloff.

Lastly, Wall Street analysts see significant potential upside for the ETF of nearly 40% over the next 12 months.

What Is the SMH ETF’s Strategy?

According to the fund’s sponsor, VanEck, SMH invests in the “MVIS US Listed Semiconductor 25 Index (MVSMHTR), which is intended to track the overall performance of companies involved in semiconductor production and equipment.”

VanEck also highlights that it uses a market-weighted index that favors the largest and most liquid companies in the industry, and that it invests in both U.S.-listed and global companies, “allowing for enhanced industry representation.”

Stellar Performance Despite the Selloff

My confidence in SMH stems from its impressive historical performance, which supports its potential for recovery. Even after accounting for this summer’s selloff, the fund has easily outperformed the broader market over the past three, five, and 10 years.

As of the end of August, the fund has returned an impressive 22.5% over the past three years. In comparison, using the Vanguard S&P 500 ETF (VOO) as a benchmark, the broader market only gained 9.3% during the same period.

Looking at the past five years, SMH has generated a scintillating annualized return of 34.8%, once again outshining the broader market, where VOO returned just 15.9%.

Over the past decade, SMH’s annualized return of 26.6% easily trumps the broader market’s return of 12.9%, reaffirming its long-term strength.

Looking at it from a cumulative perspective, SMH has created incredible wealth for its holders over the long term. For example, an investor who put $10,000 into SMH three years ago would have $16,3338 today (as of September 6). An investor who put $10,000 into SMH five years ago would have a position worth $37,435 today, more than tripling their money. Lastly, an investor allocating $10,000 into SMH 10 years ago would have an incredible $92,642 today, a return of over 900%.

SMH is a star performer that has tripled the return of the broader market over the past three years, and doubled its returns over the past five and 10 years. It’s hard to understate how strong that track record is, which gives me confidence in SMH’s potential to bounce back from the current weakness and return to winning ways.

SMH’s Portfolio

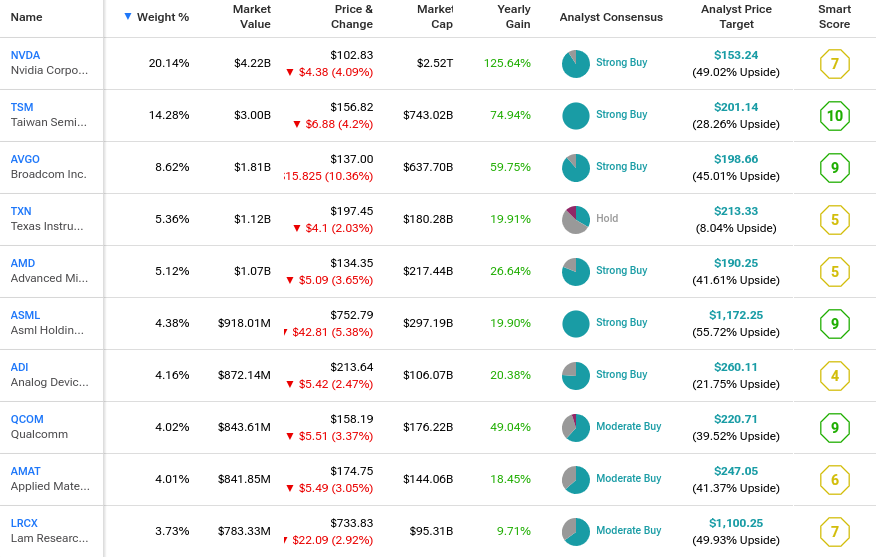

The strength of SMH’s portfolio further supports my positive outlook. SMH holds 25 stocks, and its top 10 holdings account for 73.8% of the fund.

It is not a very diversified fund. Instead, it gives investors significant exposure to some of the top stocks in the semiconductor space.

Below, you’ll find an overview of SMH’s top 10 holdings using TipRanks’ holdings tool.

As you can see, SMH gives investors significant exposure to well-known mega-cap semiconductor stocks like Nvidia (NVDA), Taiwan Semiconductor (TSM), and Broadcom (AVGO).

A large part of the reason semiconductor stocks sold off this summer was that investors rotated out of growth stocks with higher multiples amid questions about their lofty valuations and broader economic concerns.

SMH’s Top Holdings Offer Attractive Valuations and Growth Potential

Following the recent market decline, many of the SMH’s key holdings now offer much more appealing valuations. For instance, Taiwan Semiconductor, SMH’s second-largest holding, is a critical player in the global semiconductor industry, producing advanced chips for giants like Nvidia and Apple (AAPL).

Taiwan Semiconductor is one of the few companies in the world with the technological capabilities to do this, and yet it trades a 23.8 times consensus 2024 earnings estimate, in line with the broader market. Plus, the stock looks even cheaper at just 18.8 times consensus 2025 estimates, well below the S&P 500’s (SPX) current valuation of 23.6 times earnings.

Other top 10 holdings like Applied Materials (AMAT) and Lam Research (LRCX), which both make equipment used in the semiconductor manufacturing process, trade for fairly modest valuations as well. Applied Materials trades for a below-market multiple of 20.5 times earnings, and just 17.8 times 2025 earnings estimates. Meanwhile, Lam Research has an off-cycle fiscal year and is an attractive stock trading for just 20.5 times 2025 earnings estimates and a downright cheap 16.0 times 2026 earnings estimates.

Furthermore, despite the selloff, the long-term growth picture for the industry still looks promising. Fortune Business Insights forecasts that the global semiconductor industry will grow from $681.1 billion in 2024 to $2.06 trillion by 2032, good for a red-hot 14.9% CAGR over this time frame.

While a long-term forecast like this must be taken with a grain of salt as a lot can happen between now and 2032, demand for semiconductors seems likely to remain strong based on the growth of areas like generative AI, data centers, high-performance computing, Internet of Things (IoT) devices, self-driving vehicles, and more.

Expense Ratio

The expense ratio of SMH is another critical factor that affects the overall investment appeal. Currently, SMH features an expense ratio of 0.35%. This means that it charges investors a fee of $35 annually for every $10,000 invested.

While this expense ratio is higher compared to some broad-market index ETFs, it is still reasonable. Given SMH’s impressive track record of outperforming the market over the past three, five, and 10 years, many investors may find the slightly higher fee justifiable if the fund continues to deliver strong performance.

Is SMH Stock a Buy?

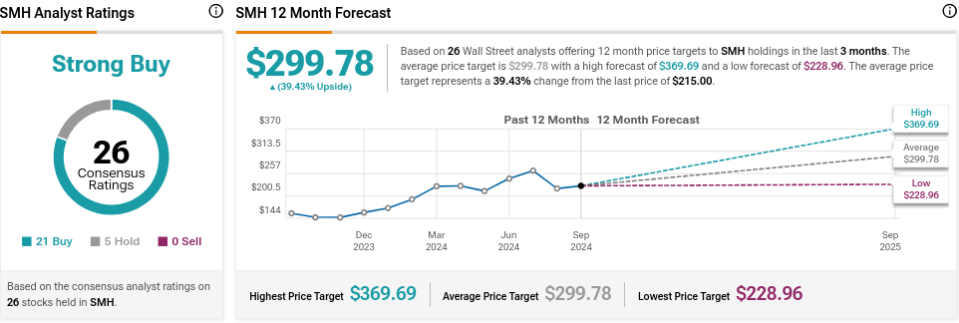

Turning to Wall Street, SMH earns a Strong Buy consensus rating based on 21 Buys, five Holds, and a zero Sell rating assigned in the past three months. The average SMH stock price target of $299.78 implies 39.4% upside potential from current levels.

Looking Ahead

After a strong start to 2024, SMH has taken a beating this summer. However, for investors with a long-term time horizon, the semiconductor sector still offers plenty of promise, and SMH is a good way to gain exposure to it.

I’m bullish on SMH based on the long-term demand picture for semiconductors, which remains intact, and the fund’s strong long-term performance, which has consistently outpaced the broader market despite the recent sell-off. Plus, Wall Street analysts view the ETF as a Strong Buy and believe it has a potential upside of nearly 40% over the next 12 months.