Royce Investment Partners Commentary: What Do Earnings, a Broadening Market and a Possible Rate ...

With less than a month to go, 3Q24 is already shaping up to be this year's most eventful quarter. First, July gave investors a significant divergence in results in favor of small-cap, with the Russell 2000 Index rising 10.2% while the large-cap Russell 1000 Index gained 1.5%. That same month also saw the Russell 2000 Value Index (+12.2%) outpace the Russell 2000 Growth Index (+8.2%). The disparity in July's returns was extreme at the extremes of market capitalization: the Russell Microcap Index advanced 11.9% while the mega-cap Russell Top 50 Index fell -0.4%.

Yet before we could breathe a sigh of relief or take a victory lap to celebrate small-cap's long awaited, though nascent market leadership, August began with a bearish wave as the globe's largest carry trade unwound when a resurgent Japanese yen led speculators to shut down bets totaling hundreds of billions of dollars across the globe. Share prices then stabilized somewhat as August went on, with small-caps down -1.5% and large-caps up 2.4%, only to fall precipitously the day after Labor Day. Amid all this volatility, we noted that the equal-weighted Russell 1000 reached a new high in August. And while we don't usually discuss the large-cap index beyond its performance, we have looked at historical data and found that when the equal-weighted Russell 1000 outperformed the capitalization-weighted Russell 1000, small-caps generally led. This makes sense to us because small-caps have generally performed at a market-leading level well when positive performance is more evenly distributed throughout the market. So, we see greater breadth in market returns as a positive sign for small-cap's relative performance prospects.

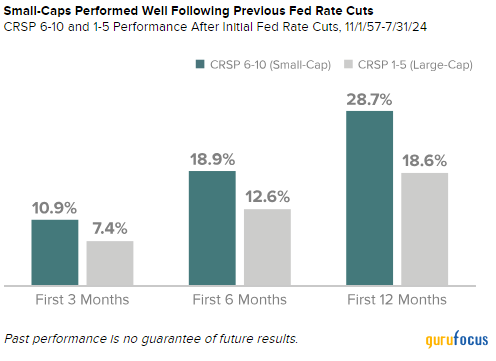

We are also anticipating that the Fed will lower interest rates later this month, though we are agnostic about the size of the reductionor its long-term effect on stock prices. However, because many observers have pinned the prospects for a sustained period of small-cap leadership to lower rates, we examined what small-caps have done following previous rate cuts. Our study took us back to November of 1957 (Fed Funds rate data goes back to July of 1954, with the first cut in 1957). As we always do when looking farther back than the 12/31/78 inception date for the Russell 2000 and Russell 1000, we used the Center for Research in Security Prices 6-10 (CRSP 6-10) and CRSP 1-5 Indexes as our respective proxies for small- and large-cap stocks. The chart below shows that small-caps beat large-caps in the 3-, 6-, and 12-month periods following Fed rate reductionsand averaged double-digit returns in each period.

We think that this history is important to balance versus the current context of the rate reductionwhich in all likelihood will be made against the backdrop of a healthy U.S. economyand certainly a non-recessionary one. In other words, the Fed is not seeking to jump start a moribund economy with a rate cut.

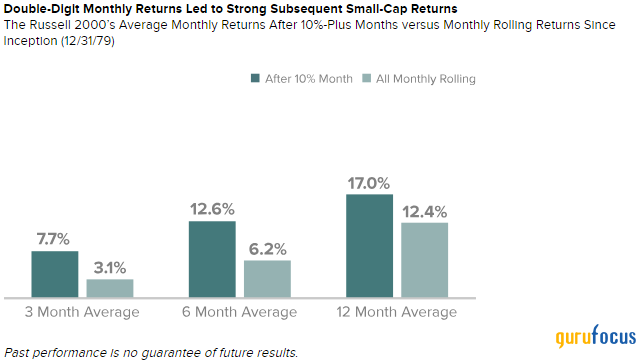

We think another context is equally important. July's 10%-plus return for the Russell 2000 is rare. The small-cap index has seen only 22 months with a double-digit return since its 12/31/78 inception. As was the case following rate cuts, the average subsequent 3-, 6-, and 12-month returns for small-caps following a 10% or higher monthly performance were impressiveand well above the Russell 2000's monthly rolling averages, as can be seen in the chart below.

Time will tell, of course, but we are highly encouraged by what history and the current economic and market environment suggest about the potential for small-cap to hang on to market leadership.

Stay tuned

Mr. Gannon's thoughts and opinions concerning the stock market are solely his own and, of course, there can be no assurance with regard to future market movements. No assurance can be given that the past performance trends as outlined above will continue in the future.

This article first appeared on GuruFocus.