Okta Stock Falls as Outlook Disappoints. Time to Buy the Dip?

Okta (NASDAQ: OKTA) shares spiraled lower after the cybersecurity company reported solid second-quarter results but offered a disappointing outlook.

On the face of it, the latest numbers looked good. Okta's Q2 revenue jumped 16% year over year to $646 million, while subscription revenue climbed 17% to $632 million. Adjusted earnings per share (EPS) surged from $0.31 a year ago to $0.72. The company had guided for 13% to 14% revenue growth and adjusted EPS between $0.60 and $0.61.

Let's catch up on the company's recent results to see if the decline is a buying opportunity.

Solid quarter, weak outlook

Looking ahead, the company's remaining performance obligation (RPO) backlog rose by 16% to $3.51 billion. Its current RPO (cRPO) backlog, which is subscription backlog expected to be recognized over the next 12 months, increased 13% to nearly $2 billion. Both of these metrics are based on signed contracts and are an indication of future revenue.

Okta's net dollar retention rate, which is how much revenue came from existing customers over the past 12 months, was 110%. That was similar to the 111% it posted last quarter. The company ended the quarter with 19,300 customers, up from 19,100 at the end of Q1. Customers with annual contract values (ACVs) over $100,000 came in at 4,620, up from 4,550 at the end of Q1.

Management has forecast fiscal 2025 third-quarter revenue to be between $648 million and $650 million, representing year-over-year growth of about 11%, and adjusted EPS of $0.57 to $0.58. It is looking for the current subscription backlog to grow by about 9% to a range of $1.985 billion to $1.99 billion. Its Q3 cRPO forecast is one area where investors seemed concerned, but that is not the only area of growth it likely will see in the upcoming year, as it will still be able to sign new deals and has upsell opportunities.

For its full fiscal year, the company forecasts revenue of between $2.555 billion and $2.565 billion, representing around 13% revenue growth at the midpoint. Adjusted EPS is expected to come in between $2.58 and $2.63. Previously, the company guided for full-year revenue of $2.53 billion to $2.54 billion and adjusted EPS in the range of $2.35 to $2.40.

This was the second straight quarter Okta that raised its guidance and the second time it was not good enough for investors. The company said it was being conservative given the macro environment and the potential impact of last year's security incident. In 2023, Okta's customer support system was hacked and data stolen from customers who use the system. It was not the best look for a cybersecurity company.

Still, Okta said there are lots of really good things going on and that it was seeing strength with large enterprises. Meanwhile, it is set to introduce a number of new products at its annual Oktane conference in October.

Should investors buy the dip?

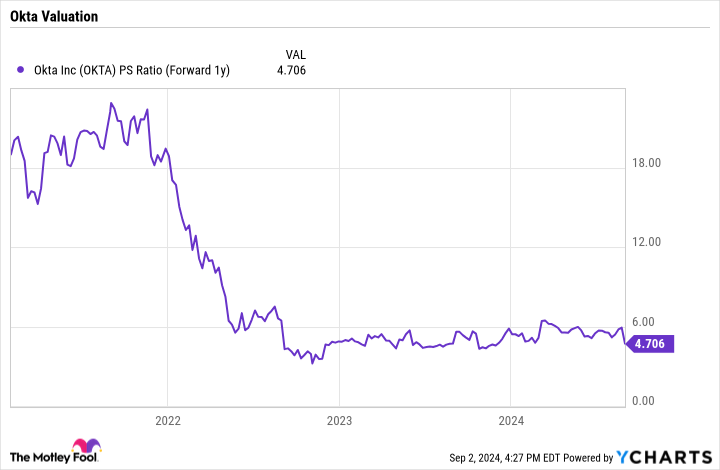

Following the recent plunge in its share price, Okta now trades at a forward price-to-sales (P/S) ratio of less than 5. This is well below that of many of its cybersecurity peers, as well as much lower than where it had traded prior to 2022. With slower growth comes a lower multiple, but I do not think its current valuation is reflective of the growth it has been generating.

As such, I think the sell-off looks overdone. The company has continued to put up solid results and appears to be taking a very conservative approach with guidance. However, investors have worried about the company's growth for a while now, and a conservative forecast does not help ease those concerns.

First, investors were worried about the impact that Microsoft and its bundling identity solutions with its 365 offering would have on Okta. Then investors became concerned about the impact of the security incident. These worries are why the company does not seem to get the benefit of the doubt from investors.

However, at Okta's current valuation and with guidance likely conservative, I think this is a pretty good spot to pick up shares.

Should you invest $1,000 in Okta right now?

Before you buy stock in Okta, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Okta wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $661,779!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 3, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Microsoft and Okta. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Okta Stock Falls as Outlook Disappoints. Time to Buy the Dip? was originally published by The Motley Fool