In This Article:

(Bloomberg) -- Just Eat Plc, the British food-delivery star of recent years, has missed out on its peers’ stock gains since entering the blue-chip FTSE 100 Index in late 2017.

“The market has been spooked by the extra investment to launch delivery services,” Ian Whittaker, an analyst at Liberum, said in an email. “More generally, there have been concerns that the food-delivery business is seeing powerful entrants,” as well as worries over the company’s recent sales decline in Australia, he said.

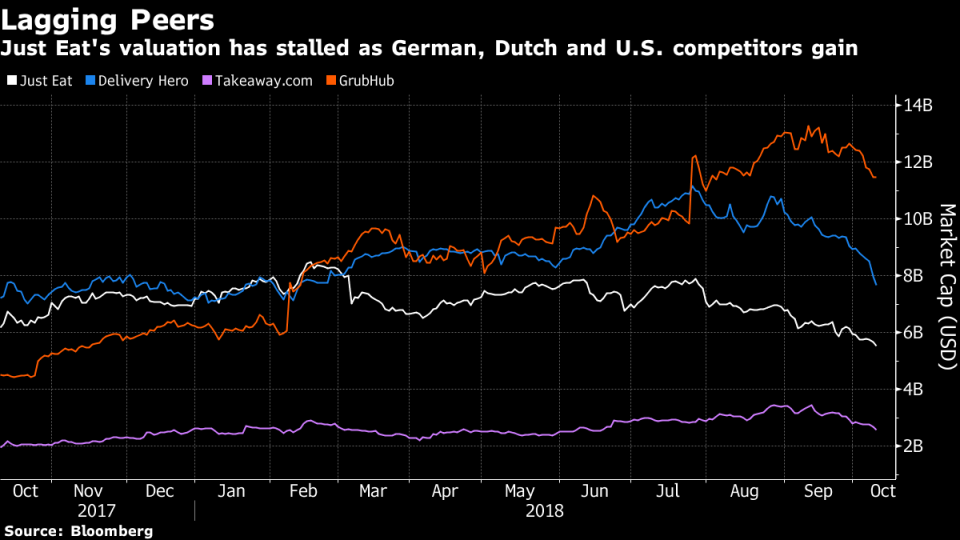

After starting the year as the most valuable online food-delivery company, Just Eat now has about half the worth of U.S. counterpart GrubHub Inc., while shares of European competitors Takeaway.com NV and Delivery Hero SE have also increased, even after coming down from mid-year peaks.

Investor sentiment started souring when Just Eat announced in March that it will spend about 50 million pounds ($65 million), more than analysts had predicted, to expand its online marketplace into a courier service. The move marked a significant change in strategy, and in July the London-based company bumped up the spending figure by 5 million pounds to 10 million pounds.

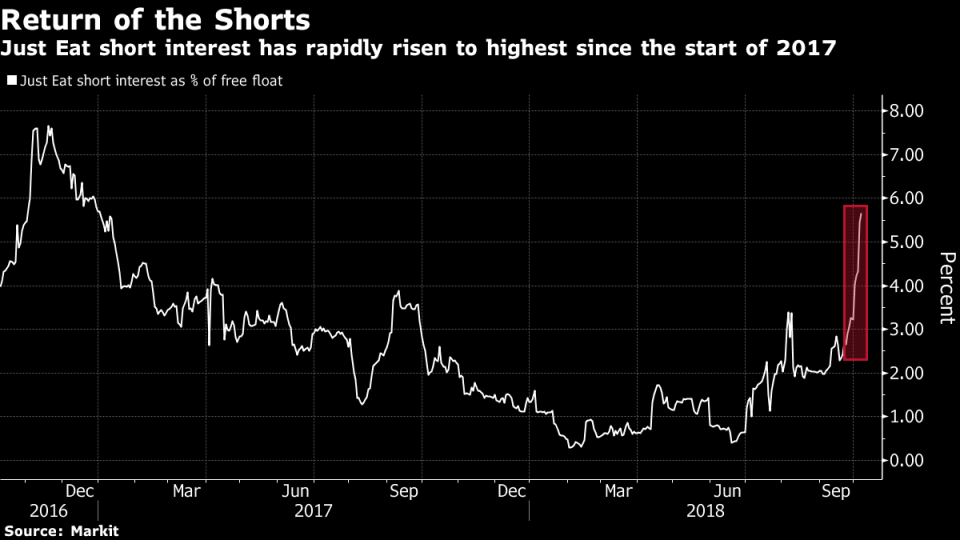

U.S. technology giants are also starting to breathe down its neck. The stock was most recently hurt by reports last month that Uber Technologies Inc. is looking to step up competition with a tie-up or purchase of London-based rival Deliveroo. Those companies provide third-party drivers for bringing meals to customers, unlike Just Eat’s predominantly online platform for restaurants with their own delivery services.

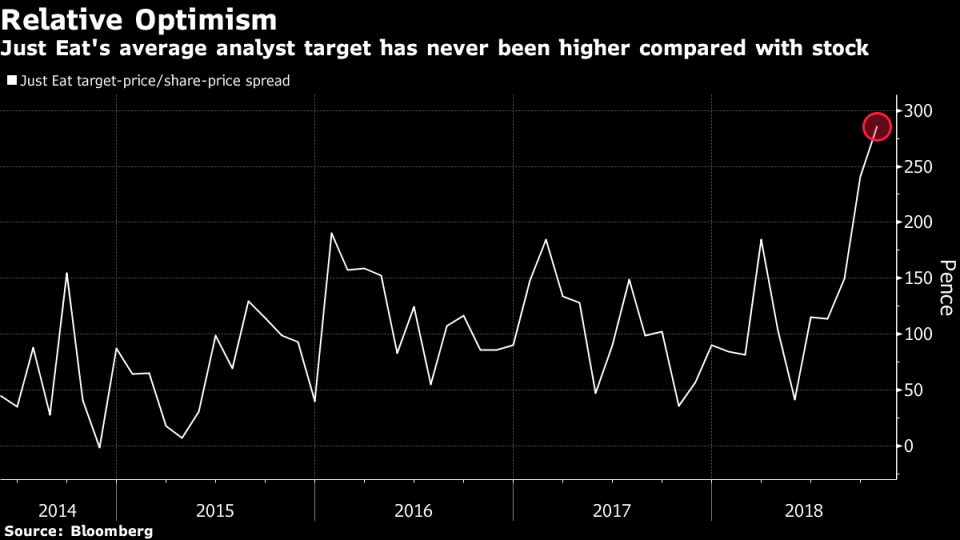

Just Eat tripled in value between its 2014 initial public offering and its graduation to the U.K. benchmark gauge, but since then the stock has progressed more slowly than the competition on many metrics. Analyst optimism hasn’t faded as quickly, and the gap between Just Eat’s share price and estimates has never been larger.

Uber Eats has in the past few months overtaken Just Eat as the top-ranked food and drink mobile application in the U.K., both in Apple Inc.’s App Store and Alphabet Inc.’s Google Play, according to download data compiled by App Annie. More than half of Just Eat’s orders are done via the app, and practically all of its profit comes from the U.K. business.

“As a result of its delayed move into delivery, Just Eat’s core customer base in terms of restaurants is still very much skewed toward the lower price segment, which increasingly brings strategic disadvantages,” Marcus Diebel, an analyst at JPMorgan Chase & Co., wrote in a report last month.