Should Investors Buy the Okta Dip?

Okta Inc. (NASDAQ:OKTA) reported second-quarter 2025 earnings last month, delivering a beat-and-raise performance. Despite this, the stock experienced a sharp sell-off, dropping nearly 20%. In this discussion, I will delve into the factors that likely contributed to this decline and offer perspective on whether the current price level presents a buying opportunity.

Near-term prospects

Okta specializes in ensuring the right people have access to the right technology at the right time. They achieve this through two main products: the Workforce Identity Cloud and the Customer Identity Cloud.

The Workforce Identity Cloud is primarily for internal company use. Employees and contractors use it to log in securely and easily to all the apps they need for work. It is like having one key that digitally opens all the doors you need in a building.

Powered by Auth0, the Customer Identity Cloud product helps companies manage how their customers log into services, ensuring that only the right users get access, and their experience is smooth, whether on the web or a mobile device.

Source: Okta Investor Relations

In simple terms, Okta helps companies manage digital identitieswho can access whatso that everything is secure and efficient. Developers also use the company's tools to build secure login systems into their own apps without starting from scratch. Okta's platform integrates with various software and applications, making it easier for companies to manage user identities.

In the near term, the company faces significant challenges, particularly from increasing competition and recent security incidents.

Revenue growth and key metrics

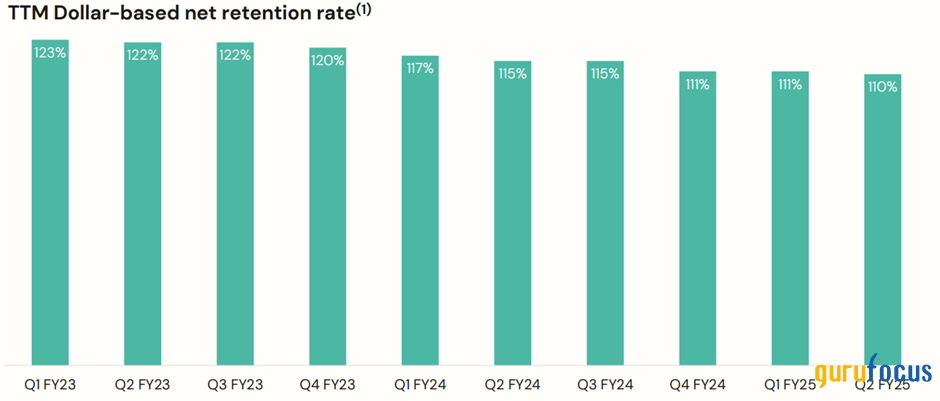

Okta has demonstrated impressive growth in key financial metrics, with total revenue growing from $399 million in 2019 to $2.45 billion in the last 12 months, representing a 39% compound annual growth rate . However, the company's dollar-based net retention rate, while still above 100%, has trended downward from a peak of 124% in fourth-quarter 2022 to 110% in the second quarter of 2025, indicating some slowdown in revenue retention.

Source: Okta Investor Relations

The net retention rate is crucial because it measures how much revenue the company is keeping and growing from existing customers over time. This downward trend is the first yellow flag in my thesis. In my opinion, this trend is primarily due to the breaches Okta had in the past. Okta faced two significant incidentsone in January 2022 involving a third-party service provider and another in October 2023 when a threat actor gained unauthorized access to its third-party customer support system, which harmed the company's reputation and customer relations. These incidents coincided with the start of the drop in the net retention rate. The full implications of these breaches are yet to be seen, but they have undoubtedly impacted customer trust.

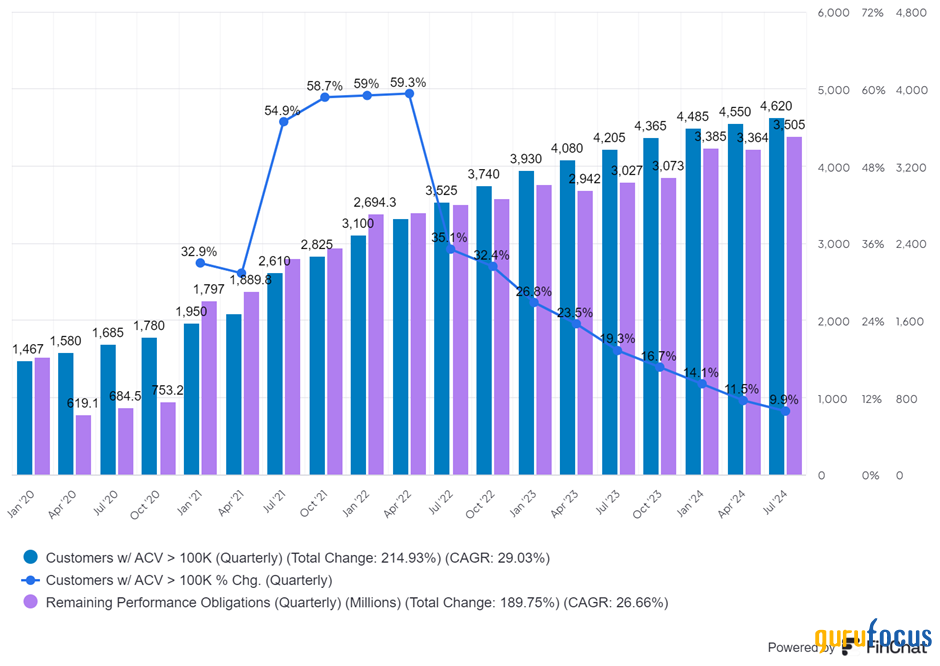

Moving to Okta's financial health, the customer base has expanded significantly, particularly among high-value accounts. Customers with annual contract values exceeding $100,000 grew from 4,205 in the second quarter of 2024 to 4,620 a year later, marking a 10% year-over-year growth rate. Despite this, the company's revenue growth rates have decelerated in the first half of 2025. More concerning is the guidance for the current remaining performance obligation, which is expected to grow by only 9%. CRPO is a good indicator of future revenue, and such a sharp deceleration suggests a challenging road ahead.

Source: FinChat

While there were some positives this quarter, such as an improvement in RPO growth outpacing CRPO, the overall picture remains challenging. A faster growth in RPO compared to CRPO could indicate Okta is securing more long-term contracts, where a larger portion of the revenue will be recognized after the next 12 months. This might signal a turning point where the net retention rate bottoms out and customer trust in Okta begins to recover.

Another positive point this quarter was Okta's GAAP net income that turned positive, primarily due to high interest income from its solid balance sheet and a net cash position of $1.24 billion, along with a $17 million benefit from income taxes.

Goodwill concerns post-Auth0 acquisition

Okta has a history of making strategic acquisitions to widen its capabilities and market reach, but the effectiveness of these capital allocation decisions remains to be seen. The company's acquisition of Auth0 allowed it to expand into customer identity management. However, a major concern regarding this acquisition was the $6.50 billion price tag, of which $5.40 billion was considered goodwill. In recent quarters, Okta has had to write down a significant portion of this goodwill because the anticipated benefits, such as revenue growth or cost synergies, did not fully materialize.

Additional risks and challenges

Adding fuel to the fire, Okta faces significant near-term challenges, particularly from the rationalization of software spending by organizations, which could impact its future revenue pipeline. Management has highlighted two primary factors underpinning its guidance.

First, the company still faces a difficult macroeconomic environment. Sluggish economic growth has forced many global corporations to slash IT spending, shrinking Okta's short-term addressable market. The high customer concentration in SMBs has exacerbated the macroeconomic impact.

Second, there are potential lingering effects from the October 2023 security incident. Third-quarter guidance indicates sales may rise less than 1% sequentially from second-quarter results, while adjusted profits could see a significant sequential decline. Although full-year 2025 projections were raised, the increase was only slightly larger than Okta's second-quarter beat, suggesting it does not have strong confidence in maintaining its positive momentum going forward.

Moreover, competition is fierce, with major tech players like Microsoft (NASDAQ:MSFT), Oracle (NYSE:ORCL) and IBM (NYSE:IBM), as well as smaller competitors like Ping Identity and OneLogin, vying for market share. Increasing competition from Microsoft Azure Active Directory, which bundles identity management with its broader software ecosystem, poses a serious threat to Okta's market share.

Valuation

Okta's valuation metrics reflect a company with significant growth potential, but the growth is slowing in the short to medium term. The company has guided for total revenue growth of 13% for fiscal 2025 and analysts expect $2.84 billion in total revenue for fiscal year 2026, implying an 11% year-over-year growth rate. The company's non-GAAP earnings per share guidance centers around a midpoint of $2.61 for this year. Analysts are expecting non-GAAP earnings of $2.89 for fiscal 2026, which reflects a higher growth rate than revenue. Nevertheless, this implies a forward non-GAAP earnings per share of 27 times and a PEG ratio of 2.49, a high valuation for a stock with so many challenges ahead.

Moreover, shareholder dilution is a concern. The current diluted weighted average share count was 174 million, reflecting a 7% year-over-year dilution rate. Management guides for a diluted weighted average share count of 182 million for fiscal 2025, indicating another 11% year-over-year dilution rate.

Conclusion

Passwordless authentication is the future, and I still believe Okta has a strong ecosystem built around its identity management platform, creating real demand for its products. However, there are currently many challenges that it needs to address before it becomes appealing for me to open a position. The sluggish economy, potential impacts from last year's security incident and a PEG ratio of 2.49 do not make the stock attractive. In my view, the potential reward does not compensate for the risks associated with the company.

The company's revenue growth is slowing significantly, and its forward guidance suggests further deceleration. While Okta's fundamentals, such as a strong cash position and achieving profitability for the first time, are positives, they do not justify the premium valuation given the challenges ahead. For now, I will continue to monitor the situation to see how management navigates these obstacles.

This article first appeared on GuruFocus.