This High-Flying Financial Stock Beat the S&P 500 in the First Half of 2024. Is It Still a Buy?

The S&P 500 delivered a 15% return for investors in the first half of 2024. This is a solid return, no doubt, but the powerhouse automotive insurer Progressive (NYSE: PGR) has trounced the index, returning investors 31% in the first six months of this year.

Progressive has a long history of outperformance relative to the benchmark index and is an excellent example of how high-quality businesses can provide outsized returns for patient long-term investors. Here's why Progressive can continue delivering for investors for years to come.

Progressive dominates in one of Warren Buffett's favorite industries

The insurance industry isn't terribly exciting, but Berkshire Hathaway CEO Warren Buffett loves investing in it, which is reason enough that we should pay attention to it. Buffett likes the steady cash flow insurers generate, thanks to the ongoing demand for insurance from individuals and businesses.

Insurance is necessary for people and businesses to protect themselves from catastrophes and is often required for legal or financial reasons. The best insurers balance the risks of holding a large pool of policies with the rewards of an underwriting profit. However, insurance is a hyper-competitive industry that makes it difficult for companies to stand out.

When you take the insurance industry as a whole, insurers, on average, tend to break even when you compare the ratio of premiums paid out to the costs of claims and expenses of running their businesses. Progressive is in a league of its own when it comes to this.

Since going public in 1971, Progressive has had a long-standing commitment to achieve a combined ratio of 96%, meaning it would earn $4 in profit for every $100 in insurance premiums it received. The company has accomplished this goal every single year since 2000 -- an impressive feat that has driven solid growth and even earned it the respect of Buffett and longtime partner Charlie Munger.

Solid performance in a tough operating environment

Over the last couple of years, insurers have grappled with inflation, which increased the cost of repairs and replacements. Claims costs rose, and underwriting profitability suffered as a result. Early last year, automotive insurers posted their worst loss ratio in two decades, and the industry combined ratio was 104%, the highest since 2017.

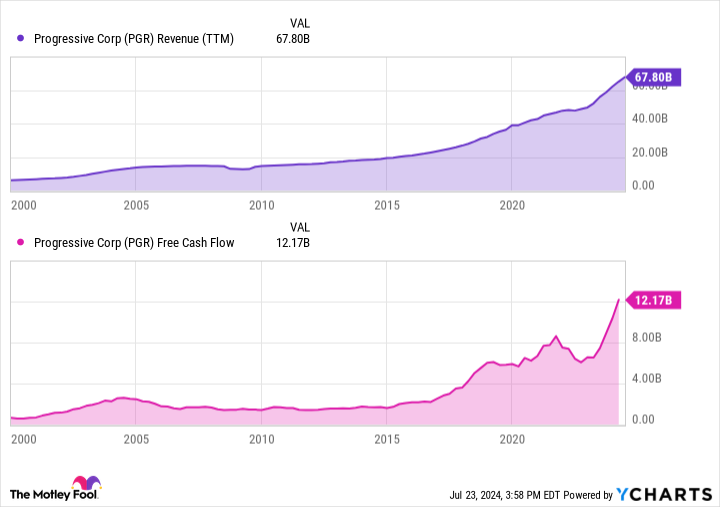

Progressive's stellar underwriting was on display again, as the insurance adjusted its premiums charged and shaped its insurance portfolio to achieve a solid combined ratio of 94.5%. This stellar performance has carried over to this year. The insurance giant has achieved an impressive combined ratio of 89.1% through the first six months, which is a big reason why the stock has delivered great returns in 2024.

An excellent stock to own across economic cycles

Progressive is a high-quality insurer that has spent decades shaping and refining its insurance book. The company was one of the first to use telematics, or driver data, to price insurance policies. That's just one example of its commitment to technology to maintain an edge over its peers.

It has performed well across various market cycles, and can be an excellent stock to own in today's uncertain economic environment. While inflationary pressures have come down, based on the year-over-year change in the Consumer Price Index, there are concerns that inflation could stay elevated compared to the last four decades.

For example, JPMorgan Chase CEO Jamie Dimon recently told investors:

There are still multiple inflationary forces in front of us: large fiscal deficits, infrastructure needs, restructuring of trade, and remilitarization of the world. Therefore, inflation and interest rates may stay higher than the market expects.

If that's the case, Progressive is well-positioned to continue its solid growth. The company has already shown its ability to adapt to inflationary pressures that emerged over the past few years, and it can grow during times of economic growth or inflation. Its policies in force continue to grow despite raising premiums, which is a testament to the company's pricing power.

The insurer also has a $72 billion investment portfolio, primarily invested in Treasuries and shorter-dated debt instruments. Progressive takes a conservative approach to its investment portfolio, and many of its debt investments are shorter-dated. It's well-positioned to earn additional investment income if interest rates remain higher over the long run, giving investors another reason to hold on to the stock for the long haul.

Should you invest $1,000 in Progressive right now?

Before you buy stock in Progressive, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Progressive wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $688,005!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. Courtney Carlsen has positions in Progressive. The Motley Fool has positions in and recommends Berkshire Hathaway and JPMorgan Chase. The Motley Fool recommends Progressive. The Motley Fool has a disclosure policy.

This High-Flying Financial Stock Beat the S&P 500 in the First Half of 2024. Is It Still a Buy? was originally published by The Motley Fool