From Guyana to the Permian Basin: How Exxon Mobil Is Positioning for the Future

Exxon Mobil Corp. (NYSE:XOM) is an energy sector powerhouse that works with immense resources and strategic investments to propel its growth for the long term. In an ever-changing market landscape, the stock brings stability and resilience to any type of investor.

A decrease in oil prices following the conflict in Ukraine meant that revenue decreased in 2023 compared to 2022, but Exxon Mobil has continued to maintain its strong financial position as well as open up new growth opportunities. A strong balance sheet and cash on hand has allowed the company to increase its dividends for a record 41st year in a row. It also reversed four quarters of declining profits in the second quarter of 2024, which is impressive considering demand has been down this year.

The company is the forerunner in the emerging Guyanese oil market and has increased its foothold domestically through strategic acquisitions in the Permian Basin. Exxon Mobil is mobilizing its resources toward the research and development and production of sustainable fuel initiatives to hedge against the real risk of climate change and the public's ever-increasing desire to move away from fossil fuels into renewable energy. How ExxonMobil will manage its global strategic initiatives as well as develop additional businesses to support the alternative fuel industry will determine its future growth story.

Financial analysis

The second quarter marked a turn after four consecutive quarters of declining revenue. 2023 was a year of reversion from the high revenue earned during 2022 that was primarily driven by the surge in oil prices due to the Russia-Ukraine war. Oil's inelastic demand allowed large corporations to generate higher revenue despite the increase in price. In the aftermath of the protracted nature of the conflict, oil prices reverted back to the levels seen in 2021, hovering in the $70 to $90 range. This brief drop in price resulted in decreased revenue for all major players.

What worked in Exxon Mobil's favor was it has been able to generate higher revenue as well as decrease expenses compared to its performance in 2021, when commodity markets were similarly priced. The company has employed prudent financial management, exponentially decreasing its short-term debt over the last three years without adding on any in 2023. The company has increased its cash balances, driven by a strong year in 2022. The company has enough cash on hand to cover its long-term debt obligations and has a strong asset base that will allow it to take on additional debt in case potential business opportunities arise in the future.

Evidence of a strong balance sheet can be seen when analyzing ratios that are relevant for the oil and gas industry. The interest coverage ratio for the second quarter was 50.42 and 62.17 for fiscal 2023, implying Exxon is more than capable of covering its debt obligations. The long-term debt-to-equity ratio was 0.13, where the industry standard ranges from 0.10 to 0.40. The company has a decreasing portion of long-term debt due for each of the next four years. This is crucial for Exxon as it is undertaking multiple developmental projects over the course of the decade. It is well-positioned to take advantage of low debt obligations over the near-term horizon, which will allow the company to act aggressively in order to get new projects functional.

Free cash flow is an important metric to use while analyzing oil companies as it is not vulnerable to volatile earnings year over year and incorporates the capital expenditure component, which is huge for oil giants. The ratio for price-to-free cash flow per share was 13.69, which is similar in levels to its peers (15 for Chevron (NYSE:CVX) and 7.30 for Shell (NYSE:SHEL)). This indicates the company is not overvalued at its current level.

Stock performance

The stock performance of Exxon Mobil along with its industry peers has been stagnant since breakout levels were achieved during 2022. The upward swing was largely driven by the crises experienced at the start of 2022. Since then, the stock has tapered off, possibly due to the fall in revenue and net income in 2023. Investors may have seen this as an indicator that operations had returned to normalcy.

The decline in revenue did not lead to a fall in price, though. A key reason for this could be that, as mentioned, revenue increased and expenses decreased compared with 2021 and the consistent payment of a dividend from management might have assuaged fears of a sell-off for investors. From an economies of scale perspective, this is impressive. To increase earnings by 20% (comparing 2021 to 2023) is not an easy task for an enterprise as large as Exxon. This may be the reason why investors are hesitant to sell the stock post the highs reached in 2022. The price of crude may have cooled off, but the company's ability to generate substantial growth under normal market conditions may have directed investors away from selling.

Exxon Mobil has a history of increasing dividend payments stretching back 41 years. In addition to this, a $17.50 billion share repurchase plan bodes well for long-term investors. Even if the stock had not appreciated since 2022, dividends have, and although a shareholder loses out on capital appreciation, he gains greatly through dividends. A large share buyback program is usually a good indication that management is doing something right and that they would happily exchange cash for buying back more stock. This is an exciting prospect for a long-term shareholder, but it also injects fresh cash into the company that can be diverted away to the best possible use. This could indicate there is large growth potential on the horizon and the company believes more cash on hand is critical for realizing those goals.

The share buyback program is also critical to keep the share price from being too volatile. As part of the merger with Pioneer Natural Resources, Pioneer shareholders received 2.3234 shares of Exxon for each share they held at closing. The buyback program can counter the effect of new Exxon shares created through the merger that would depress the share price.

Currently, Exxon is valued at a modest price-earnings ratio of 12.82. This is a similar ratio to its industry peers as Chevron trades at 11.80 times earnings and Shell at 8.3, but also much lower than companies of similar size (in terms of earnings and market cap). Even if an investor loses out on capital appreciation due to the stagnant stock price, they would benefit from the dividends received and any future share buyback programs. Additionally, strong earnings for multiple years coupled with consistently lowering the company's debt profiles suggest that at its current price, Exxon Mobil seems to be undervalued.

The effect of ever-increasing dividends can be seen in the total return performance of 109% between Exxon and the S&P 500 over the past five years. Since the lows of the Covid pandemic, dividends have driven the performance of the stock over the index. For a company like Exxon, total return is the preferred metric to use over price return because of the dividend component.

Guyanese growth

Expansion into new markets is also benefitting the company.

Oil was discovered off the coast of Guyana in 2015 by ExxonMobil Guyana Ltd. Since then, the small country has witnessed a boom in oil production and consequently its per capita income. As such, the developing country's government welcomes the drilling projects compared to more environmentally conscious and prosperous countries like Canada. This has led to an unprecedented period of wealth for the nation, fueled by its oil production. Exxon Mobil is at the forefront of this boom as it was the first and largest producer of oil in the region. Further, the region is of great significance for the future of oil production as reserves in the Middle East and elsewhere slowly dwindle.

Guyana's energy development is supporting the fastest real gross domestic product growth in the world. With the full support of the Guyanese government to conduct drilling activities, Exxon Mobil is in a prime position to capitalize from this boom. Entering new markets can be painful for an oil company, so being the premier operator in this new market has allowed the company to break away from its peers. Global production in the second quarter surged by 21%, with Guyana contributing majorly with a gross production of 630,000 barrels per day, a record for Exxon.

The company has commissioned a sixth offshore project in Guyana with production expected to begin in 2027 and has applied to the Guyanese Environmental Agency for a proposed seventh project starting in 2029, adding to its existing impressive portfolio in the region. Despite the country not being a major contributor to non-U.S. revenue, it is the fifth-largest long-lived asset holding for the company. It is clear the company is going all hands-on-deck with the Guyanese agenda and the success or failure of this endeavor will determine Exxon's trajectory in the coming years.

Pioneer acquisition

At home, Exxon completed a significant strategic move with the acquisition of Pioneer Natural Resources, which became the largest merger in the petroleum industry in 20 years. This has significant implications for the company, doubling its portfolio in the region.

Exxon Mobil has a key strategic presence in the Permian Basin and this acquisition has made it the largest producer both in the Permian Basin and the entire U.S. In the second quarter, the company topped 1 million barrels of oil produced in the Permian, largely owing to the merger with Pioneer. The combined company's Delaware and Midland basins have an estimated 16 billion barrels of oil equivalent resources.

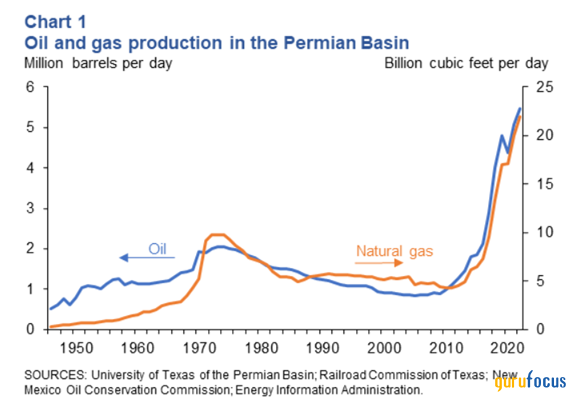

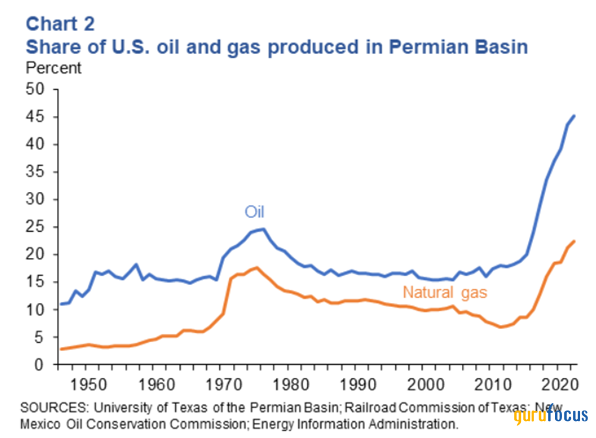

As illustrated below, the Permian Basin is the most important location for oil production in the U.S. in terms of overall output, but also as a share of U.S. oil and gas supply.

Exxon has identified possible growth opportunities at home and has capitalized on it. Small and medium-sized enterprises like Pioneer are responsible for 80% of the production from the Permian Basin, and Exxon's acquisition of the company gives it the biggest market share in an oil-rich region. Exxon stands to gain massively as a larger portion of the U.S. population depends on oil and gas produced in the area.

Outlook

Exxon has performed well over the last two years and is modestly valued based on price-earnings and price-to-free cash flow ratios. Management has continued to increase dividends year over year and has bought back shares without compromising on strategic and growth opportunities.

The company's presence in Guyana will be of immense importance in the coming years and the company's acquisition of Pioneer Natural Resources has allowed it to have the largest presence of any oil company in the U.S. Exxon Mobil has a strong balance sheet and decreasing debt obligations over the near term. Global events have a cascade effect on oil prices, so rising tensions in the Middle East, with fears of an Iranian attack on Israel, provides a floor for the price of crude. Exxon has also entered the electric vehicle market by agreeing to supply .ithium to battery manufacturers. The company is positioned strongly for the long term and global tensions can potentially be of benefit for its near-term prospects as well.

At this point, considering the modest price ratios, the strong balance sheet, earnings, increasing dividends and other critical factors mentioned above, I would suggest a long-term investor to hold or buy shares of Exxon Mobil as I believe the stock is slightly undervalued at its current price. Investors stand to gain from increasing dividends and share buyback programs. Conflicts in the Middle East have the chance of causing a ripple effect on oil prices, which can increase the share price of oil giants like Exxon Mobil in the near term. I believe the company is well positioned to tackle the challenges it will face in the future.

This article first appeared on GuruFocus.