Forget Starbucks: Buy This Other Sizzling-Hot Coffee Chain Stock Instead

As earnings season comes into full bloom, some businesses outside big tech are capturing the attention of investors.

Coffee chain Starbucks (NASDAQ: SBUX) is a closely followed company because its trends can offer unique insights into the health of the economy and consumer purchasing habits.

Last week, Starbucks released results for its second quarter of fiscal 2024, ended March 31. Overall, the report didn't leave much to be desired, and shares have cratered 14%.

Let's dig into Starbucks' earnings report and analyze why I see a different coffee chain stock as the better buy.

Challenges across the board

Analyzing retail businesses can be daunting. For starters, when a retail company reports revenue growth, it can be misleading, because investors often are not told how much of this growth is derived simply from price increases.

Moreover, considering retail businesses are constantly opening and closing locations, it can be hard to assess a company's organic growth trends. For this reason, one of the most important metrics for retail businesses is same-store sales.

Same-store sales can be seen as a more useful metric than revenue growth because it measures activity from stores that have been open for at least one year. This provides investors with an important view of the company's foot traffic, and how those trends may lead to further expansion or closures of the retail outlet in question.

For the period ended March 31, same-store sales declined by 4% year over year. Of note, comparable sales dropped both domestically in the U.S. and internationally -- including major markets such as China.

In addition to a deceleration in same-store sales, management cited another challenge during the earnings call -- and I found this one to be quite concerning. Starbucks' CEO Laxman Narasimhan admitted that the coffee chain is struggling to spur demand other than a daily influx of morning commuters.

Where is the loyalty going?

Over the last couple of years, inflation has been unusually high. As a result, the Federal Reserve has instituted a number of interest rate hikes. The combination of higher prices and rising borrowing costs have undoubtedly weighed on consumer pricing power.

One area where Starbucks may be losing some momentum is value. I think that Starbucks is falling behind with consumers due to its prices. Although prices of goods and services have risen across the board over the last couple of years, Starbucks is perceived as a luxury brand -- and its food and drinks are expensive compared to alternatives.

A smaller chain called Dutch Bros (NYSE: BROS) has demonstrated some impressive growth over the last few years, and I suspect that some coffee enthusiasts are opting for this in lieu of Starbucks.

For the period ended March 31, Dutch Bros reported that same-store sales rose 10% year over year. Moreover, revenue for the quarter increased 40% year over year. By comparison, Starbucks' revenue growth during the quarter was flat.

Given the robust operating results, Dutch Bros raised its full-year 2024 revenue and profit guidance. Unsurprisingly, this is much different than Starbucks, which lowered its guidance following the poor earnings tape.

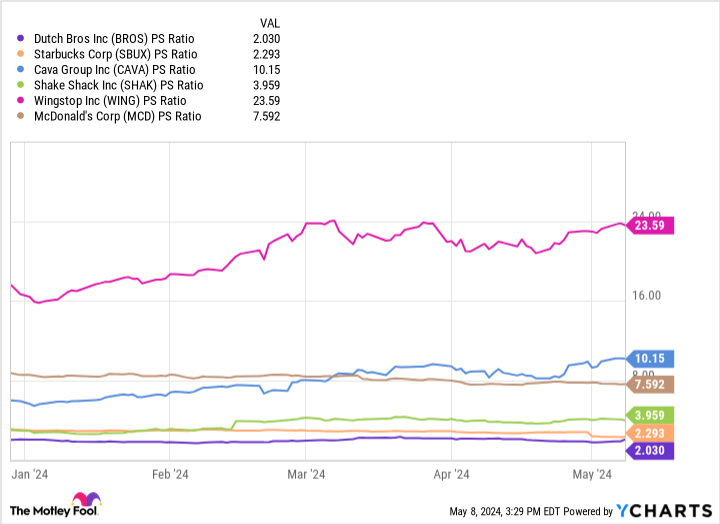

Is Dutch Bros stock a buy right now?

The chart benchmarks Dutch Bros against a cohort of restaurant-adjacent companies. With a price-to-sales (P/S) multiple of 2, Dutch Bros is the least expensive stock in the peer set based on this measure.

While this might appear as if Dutch Bros is dirt cheap, I'd caution investors from such thinking. While Starbucks is facing some headwinds at the moment, it is still a much larger and financially robust operation. And yet when looking at the P/S multiples above, Dutch Bros is actually in line with Starbucks.

However, considering the company's organic growth and positive outlook, I think the premium is warranted for Dutch Bros. Generally, for any retail business, the biggest challenge will be expansion. For now, Dutch Bros is largely a West Coast operation. Considering Starbucks has locations in 80 countries, Dutch Bros has a long way to go before it reaches commensurate scale.

I think investors that are looking for some growth opportunities outside the obvious sectors such as technology, healthcare, or energy may want to consider Dutch Bros. As far as consumer discretionary businesses are concerned, the company has established itself as more than a niche player. While the stock might be a little pricey at the moment, I think long-term investors will still reap considerable upside.

Should you invest $1,000 in Dutch Bros right now?

Before you buy stock in Dutch Bros, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dutch Bros wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $550,688!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 6, 2024

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Starbucks and Wingstop. The Motley Fool recommends Cava Group. The Motley Fool has a disclosure policy.

Forget Starbucks: Buy This Other Sizzling-Hot Coffee Chain Stock Instead was originally published by The Motley Fool