Fed’s Powell Nods to Upcoming Strategy Review as Officials Prepare to Cut Interest Rates

(Bloomberg) -- In Jackson Hole this weekend, Federal Reserve Chair Jerome Powell outlined two priorities for the months ahead: keeping the US economy afloat while also taking a closer look at what went wrong over the past few years.

Most Read from Bloomberg

Sydney Central Train Station Is Now an Architectural Destination

Nazi Bunker’s Leafy Makeover Turns Ugly Past Into Urban Eyecatcher

How the Cortiços of São Paulo Helped Shelter South America’s Largest City

Headlines from the Fed chair’s Friday speech were dominated by his concerns over the state of the cooling labor market.

But Powell also previewed what will be the Fed’s first formal review of its strategy since being caught off guard by an inflation surge during the pandemic, a mistake that forced officials to raise interest rates rapidly to catch up.

“As we begin this process later this year, we will be open to criticism and new ideas, while preserving the strengths of our framework,” Powell said at the Kansas City Fed’s annual Economic Policy Symposium, the same forum where the outcome of the last review was unveiled in 2020.

“The limits of our knowledge — so clearly evident during the pandemic — demand humility and a questioning spirit focused on learning lessons from the past and applying them flexibly to our current challenges,” he said.

In the four years since the US central bank last revamped its policy framework, it’s witnessed a once-in-a-century global pandemic, historic fiscal stimulus and multiple geopolitical crises — all of which helped propel inflation to the highest levels in four decades.

Prominent economists, former Fed officials and some Republican lawmakers have criticized the strategy, announced shortly after the onset of Covid-19 and just before prices began to soar. Critics charged that it was too narrowly focused on the single scenario of inflation running below the Fed’s 2% target, which led to it becoming quickly outdated.

Powell himself acknowledges the Fed was slow to begin raising interest rates in 2022 because he and his colleagues misjudged how persistent inflation would prove to be. A big part of the debate since then has been over whether the changes to the framework in 2020 should take part of the blame for the delay.

“It took them a while to understand the world had changed,” said Ellen Meade, a Duke University professor who was previously a senior adviser at the Fed in Washington. “They absolutely need to do a retrospective.”

US central bankers aren’t the only ones undertaking a postmortem: The European Central Bank has already begun a similar review. ECB President Christine Lagarde has said that the exercise won’t be as wide-ranging as the last one in 2021 — which marked the first in 18 years — but it nevertheless could have significant implications for future rate decisions and the ECB’s response to crises.

At the Fed, officials are likely to scrutinize how they approach each of the mandates assigned to them by Congress — low inflation and maximum employment. The framework they unveiled in 2020 was influenced by the moment: Millions of people had just been thrown out of work and inflation was still subdued after years of running below 2%.

That backdrop informed two key changes. First, the central bank would seek moderately above-target inflation following bouts of below-target inflation. And second, it would respond when the unemployment rate rose above what it considered a neutral level, but not when it fell below that level.

Notable Departure

The latter shift marked a notable departure from the longstanding approach in which the Fed would begin tightening in times of low unemployment to stem any potential inflationary pressures that may result from a hot labor market.

“We do need to sometimes raise rates before inflation takes off,” said Kristin Forbes, a Massachusetts Institute of Technology professor and former Bank of England policymaker. “They’ll have to go back to making it more symmetric of how they think about both inflation and unemployment.”

Economists have also suggested the Fed’s forward guidance may have played a role in delaying their response to rising inflation. Policymakers said in 2020 they expected to keep rates low to support the economy until they’d seen inflation moderately above 2% for “some time,” and would continue large-scale bond purchases until they’d made “substantial further progress” toward their inflation and employment goals.

How the Fed communicates its intentions to the public will also probably come in for scrutiny. Powell said in June that communications would be “within scope” of the review, while offering few details on what that could entail.

One of the main points of discussion during presentations and on the sidelines at the Jackson Hole conference was whether investors and the broader public understand the Fed’s approach, and ways they could be more effective about telegraphing how they might react under different situations.

That’s become a hot topic in central banking circles since former Fed Chair Ben Bernanke published a report in April for the BOE. In it, he recommended policymakers make greater use of such scenario analysis in their forecasting.

Fed Governor Lisa Cook and Loretta Mester, who recently retired from her post as president of the Cleveland Fed, are among US officials who have spoken favorably of scenario analysis. Improving communication can be important in the months ahead amid uncertainty over the trajectory of the labor market, Mester said.

“When the data comes in differently than you think, that will change your reaction,” Mester said in an interview on the sidelines of the conference in Grand Teton National Park. “How do you communicate that to the average person? That’s what you need to be doing.”

Different Circumstances

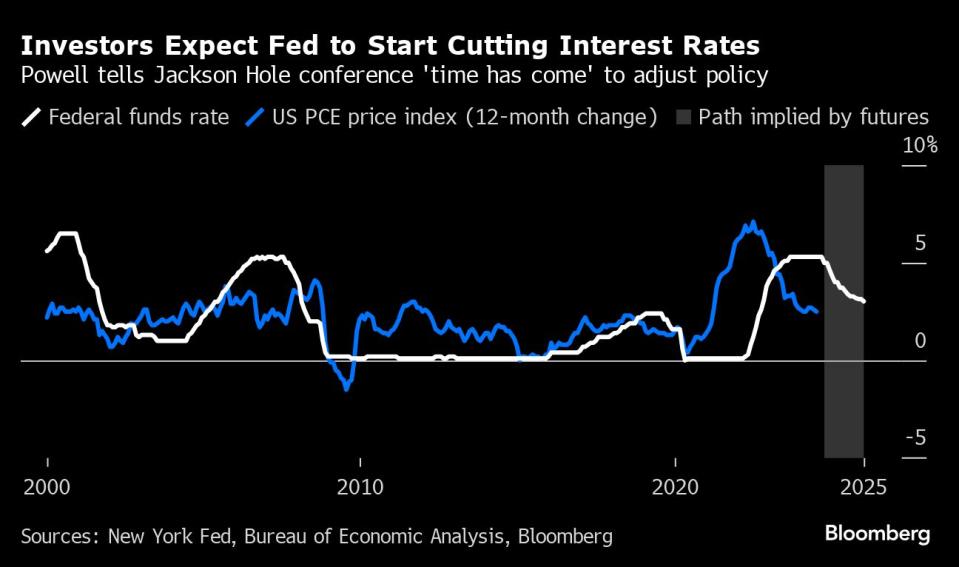

With inflation almost back to the Fed’s target and concerns over unemployment rising, the central bank is poised to begin cutting rates in September. That’s bringing questions about how quickly it needs to ease and where rates will ultimately settle into the spotlight.

Some policymakers have suggested borrowing costs may not return to the ultra-low levels of the past — contrary to the description of “likely” outcomes in the Fed’s current “Statement on Longer-Run Goals and Monetary Policy Strategy.”

The debate is over whether an investment boom in artificial intelligence, a shift in globalization patterns and more frequent supply shocks may lead to higher average rates, or if longstanding trends like demographics that have pushed rates lower over time will continue to win out.

Policymakers don’t have to agree on an answer during the review, but they may want to make a more explicit acknowledgment that they could be fighting inflation that is either above or below their target, Meade said.

“The last few years has been a wake-up call,” Forbes said. “You want to do a framework review that is robust to many different economic circumstances.”

--With assistance from Mark Schroers.

Most Read from Bloomberg Businessweek

Losing Your Job Used to Be Shameful. Now It’s a Whole Identity

FOMO Frenzy Fuels Taiwan Home Prices Despite Threat of China Invasion

©2024 Bloomberg L.P.