Discover 3 Undiscovered Gems with Strong Fundamentals

Over the last 7 days, the market has dropped 5.6%. As for the longer term, the market has risen by 12% in the last year, with earnings forecast to grow by 15% annually. In this fluctuating environment, identifying stocks with strong fundamentals can be key to finding value and stability. Here are three undiscovered gems that stand out due to their robust financial health and growth potential.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

Morris State Bancshares | 10.20% | -0.32% | 6.73% | ★★★★★★ |

San Juan Basin Royalty Trust | NA | 39.20% | 40.92% | ★★★★★★ |

Teekay | NA | -6.48% | 55.79% | ★★★★★★ |

Mission Bancorp | 25.37% | 16.23% | 20.16% | ★★★★★★ |

Omega Flex | NA | 1.31% | 3.88% | ★★★★★★ |

Gravity | NA | 15.31% | 24.42% | ★★★★★★ |

First Northern Community Bancorp | NA | 7.12% | 10.04% | ★★★★★★ |

United Bancorporation of Alabama | 13.34% | 18.86% | 25.45% | ★★★★★☆ |

CSP | 2.17% | -5.57% | 73.73% | ★★★★★☆ |

FRMO | 0.19% | 6.49% | 15.82% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

EZCORP

Simply Wall St Value Rating: ★★★★★☆

Overview: EZCORP, Inc. operates pawn services across the United States and Latin America with a market cap of $605.97 million (NasdaqGS:EZPW).

Operations: EZCORP generates revenue primarily from its U.S. Pawn segment ($818.54 million) and Latin America Pawn segment ($318.95 million). The company's net profit margin is a critical financial metric to consider when evaluating its profitability trends over time.

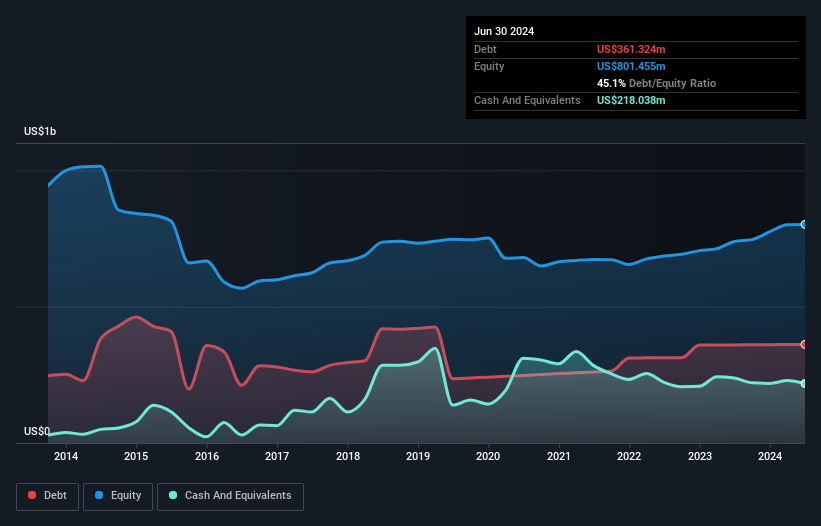

EZCORP, Inc. has shown strong financial performance with earnings growing by 119.9% over the past year, significantly outpacing the Consumer Finance industry’s -9.2%. The company's debt to equity ratio rose from 31.5% to 45.1% in five years but remains manageable with a net debt to equity ratio of 17.9%. Trading at a P/E ratio of 7.8x, it is undervalued compared to the US market average of 17.5x and demonstrates high-quality earnings and robust EBIT coverage (35.2x).

Navigate through the intricacies of EZCORP with our comprehensive health report here.

Understand EZCORP's track record by examining our Past report.

Powell Industries

Simply Wall St Value Rating: ★★★★★★

Overview: Powell Industries, Inc., along with its subsidiaries, specializes in designing, developing, manufacturing, selling, and servicing custom-engineered equipment and systems with a market cap of $1.84 billion.

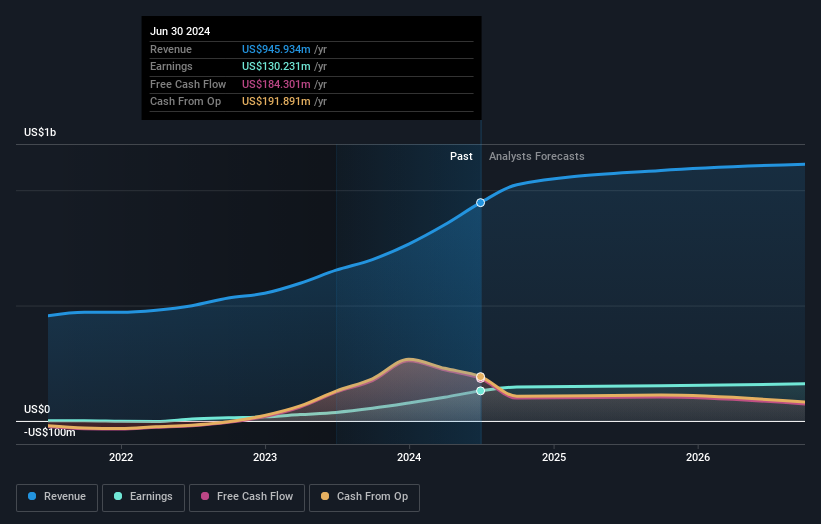

Operations: Powell Industries generates revenue primarily from its Electric Equipment segment, which brought in $945.93 million. The company has a market cap of $1.84 billion.

Powell Industries, a small-cap player in the electrical industry, has shown impressive financial performance. Its earnings grew 253.6% over the past year, significantly outpacing the industry's 19.8%. The company reported third-quarter sales of US$288.17 million and net income of US$46.22 million, compared to US$192.37 million and US$18.45 million respectively a year ago. With no debt on its balance sheet and trading at a P/E ratio of 14x versus the market's 17.5x, Powell appears attractively valued despite recent share price volatility.

Delve into the full analysis health report here for a deeper understanding of Powell Industries.

Evaluate Powell Industries' historical performance by accessing our past performance report.

Hamilton Beach Brands Holding

Simply Wall St Value Rating: ★★★★★★

Overview: Hamilton Beach Brands Holding Company, with a market cap of $266.68 million, designs, markets, and distributes small electric household and specialty housewares appliances in the United States and internationally.

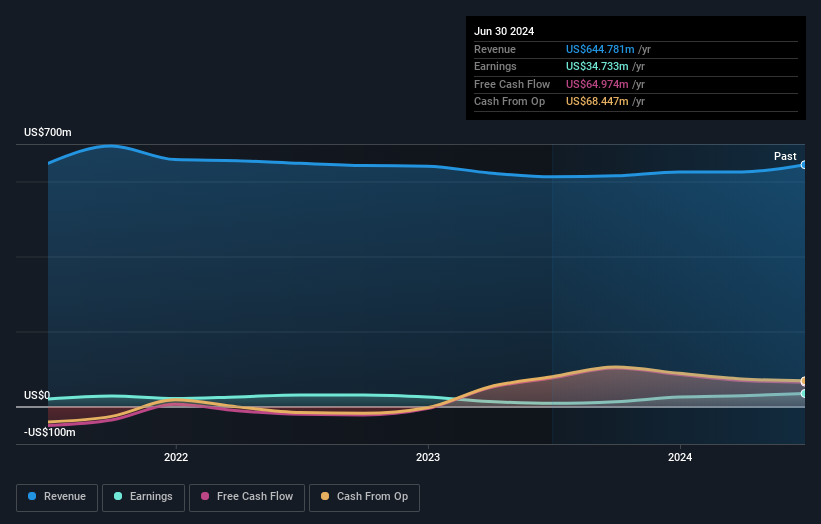

Operations: Hamilton Beach Brands Holding Company generated $644.78 million in revenue primarily from its subsidiary, Hamilton Beach Brands, Inc. The company reported a net profit margin of 3.5%.

Hamilton Beach Brands Holding has shown impressive performance recently, with net income rising from US$0.11 million to US$5.99 million in the second quarter of 2024. The company's debt to equity ratio has improved significantly over the past five years, dropping from 154% to 34.3%. Its earnings growth of 316.6% in the past year outpaced the Consumer Durables industry average of -2.6%. Additionally, HBB's interest payments are well covered by EBIT at a ratio of 40.7x, indicating strong financial health and profitability.

Make It Happen

Discover the full array of 220 US Undiscovered Gems With Strong Fundamentals right here.

Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Curious About Other Options?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NasdaqGS:EZPW NasdaqGS:POWL and NYSE:HBB.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com