Comcast Is a Large Diverse Business. But There Are 2 Simple Reasons Why I Won't Buy Its Stock.

With business operations in telecom infrastructure, media, film studios, theme parks, and more, Comcast (NASDAQ: CMCSA) is one of the largest and most diverse businesses in the world. The total market value of the company is nearly $150 billion, making it one of the largest public companies in the world as well. This combination of scale and diversity makes it an attractive investment target for many.

But it's not attractive to me. For all of its virtues, Comcast stock is one that I'm not buying. There are two simple reasons why.

1. Comcast lacks consistent growth

To be clear, growth isn't the only factor that helps stocks perform well over the long term. In fact, growth can be detrimental when it moves a business into a more competitive, lower-margin operation. But for the most part, growth is a big factor for stocks that outperform the S&P 500.

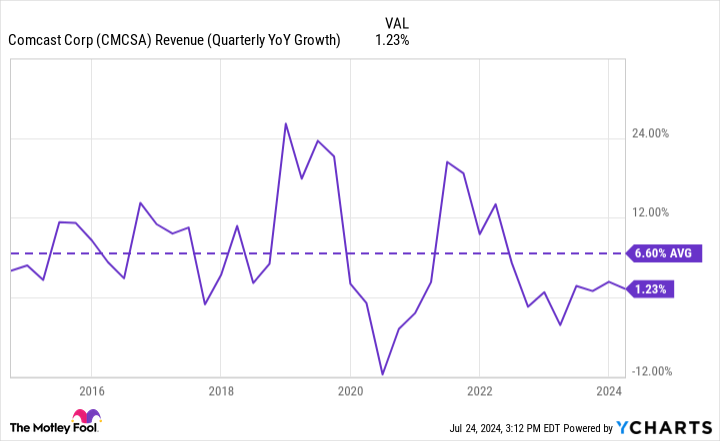

Over the last 10 years, Comcast's growth has been quite meager. Its long-term average growth rate is in the single digits, as the chart below shows.

Comcast's growth hasn't consistently impressed in a long time and its most recent results were modest as well. In the second quarter of 2024, revenue was down almost 3% year over year.

Granted, this modest slip in revenue wasn't unexpected for Comcast. The company's theme parks didn't perform as well as they did in the prior-year period. And its studio business was lapping some really successful movies last year. Investors were prepared for this for the most part.

However, the point still stands that at Comcast's scale -- over $120 billion in trailing-12-month revenue -- incremental growth is hard to come by. I expect its growth to remain modest in the coming decade. And growth is important, which is why this is one factor that keeps me on the sidelines.

2. Comcast's shareholder returns are potentially unsustainable

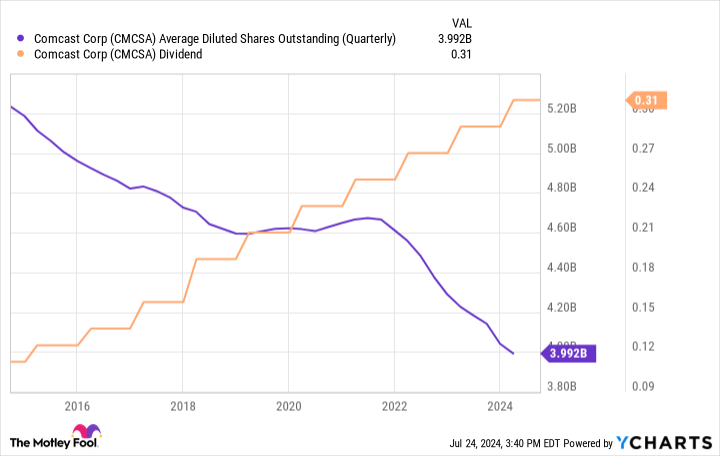

Comcast is a very shareholder-friendly company -- this is something that many investors appreciate. The company has raised its dividend every year for 16 years. And it's repurchased shares consistently, bringing its share count down by more than 20% during the last decade and increasing shareholder value.

In the absence of growth opportunities, these are sensible moves for large, profitable businesses such as Comcast. Companies either need to grow shareholder value by expanding the business or they need to give cash back to shareholders. So I don't fault management for paying a growing dividend or repurchasing shares.

However, the pace of shareholder returns could be questioned. It's customary to compare a company's free cash flow to the money it gives back to shareholders. Comcast gave 140% and 122% of its free cash flow back to shareholders in 2022 and 2023 respectively. In other words, it paid out more than it made, which is unsustainable.

This trend has somewhat continued in 2024. In the first quarter, Comcast had free cash flow of $4.5 billion and gave $3.6 billion back to shareholders, which was 80%. Adjusting to factor out a one-time tax issue in Q2, it gave back more than 100% again.

As much as it gives back to shareholders, Comcast is already doing about as much as it can. But even at this rate, it might not be enough to boost shareholder returns above the average for the S&P 500. Its dividend yield is 3% and it can perhaps reduce its share count at a single-digit annual rate. A total shareholder return of 10% annually might push the limits here.

What about those who disagree?

I've shared two reasons why I don't plan to buy Comcast stock. But every investor is different and I'm sure others might still be attracted to the company for its high-yield dividend and the stability found in the diversity of its business.

This might be true. But those looking for stability and solid dividend income might want to consider a solid dividend-paying exchange-traded fund (ETF) instead. An ETF is a collection of stocks, which provides instant diversification and relative safety. And ETFs with a dividend focus can provide consistent payouts there, too.

By contrast, long-term investors who pick individual stocks such as Comcast should try to beat the market average. Comcast's business is strong and it won't disappear tomorrow. But I don't believe it can outperform the S&P 500 from here for the two reasons I've shared, which is why it's not for me.

Should you invest $1,000 in Comcast right now?

Before you buy stock in Comcast, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Comcast wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Jon Quast has no position in any of the stocks mentioned. The Motley Fool recommends Comcast. The Motley Fool has a disclosure policy.

Comcast Is a Large Diverse Business. But There Are 2 Simple Reasons Why I Won't Buy Its Stock. was originally published by The Motley Fool