(Bloomberg Opinion) -- BlackRock Inc., the world’s largest asset manager, says it will cut exposure to companies linked to thermal coal, among other climate-friendly measures. It’s a powerful signal. Unfortunately, it only scratches the surface. If BlackRock CEO Larry Fink is serious about helping to eliminate coal while reshaping finance, his outfit can use its holdings of sovereign debt to tackle governments, too.

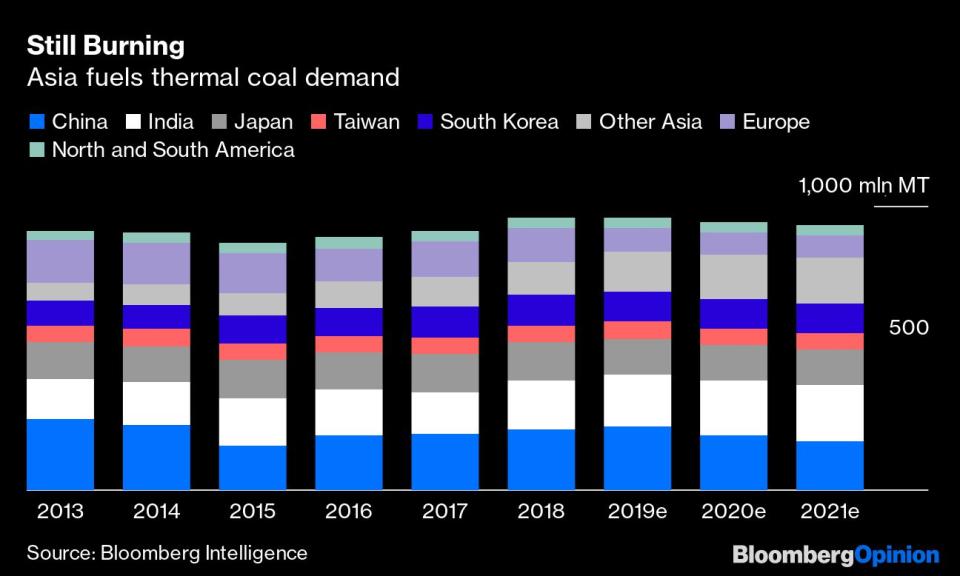

Coal power generation has fallen steeply in Europe and the U.S. in the past year or so, thanks to cheap natural gas, higher carbon prices and green pressure. Yet in Asia, once you iron out some local peculiarities, demand for the black stuff remains remarkably resilient. That suggests that even if global appetite peaks soon, as most analysts estimate, it could well remain at high levels for years to come. Analysts at UBS Group AG estimated last July that on current trends the last coal-fired power station may close only in 2079. To blame are the likes of China, India and Vietnam. Their fleet is young, still growing and often state-backed; Western money managers selling out of public securities won’t change that.

There is good news. BlackRock is an investment giant, with $7.4 trillion of assets under management, so Fink’s call to arms last week marks a significant move. Cutting off funds for coal producers and driving up their cost of capital is key to suffocating a sector that is the single largest cause of increased global temperatures.

BlackRock’s strategic shift is also driven by self-interest. That’s encouraging, as such initiatives tend to outlast moral outrage. Heat from activists, like the BlackRock’s Big Problem campaign, helped, but Fink argues he is making sustainability the new standard because it makes financial sense. The surge of inflows into the firm’s environmentally friendly funds last week will encourage that view.

The devil, as ever, is in the detail. BlackRock’s aim to divest thermal coal equity and debt will apply to its actively managed funds. Yet those amount to only under a third of the money it manages.

As worrying is the threshold to be used to determine what has to go: The fund manager will sell out of any company where 25% of revenue or more is derived from thermal coal. That gets at narrowly focused producers like Australia’s Whitehaven Coal Ltd., but leaves untouched stakes in diversified heavyweights, like BlackRock’s 6% holding in Glencore Plc, the world’s top producer of seaborne thermal coal, or other sprawling conglomerates. It also tackles primarily miners, not utilities that consume the fuel.

It’s possible to aim higher: Axa SA last year vowed to reduce its exposure to the thermal coal industry to zero by 2040.

The bigger problem is that while such moves are necessary, they aren’t sufficient. That’s firstly because of the haven offered by private markets. If a large investment fund divests a stock or bond, or pressures companies into selling out of coal projects, what next? BlackRock investors may feel better, but will global production reduce overall? Quite possibly not. Will the world be greener? Also, possibly not, if the pit is sold to owners out of the public eye. Arguably, it may become harder to monitor.

That suggests a more effective pressure point is demand, and that means tackling governments and state-backed firms still funding and supporting the fuel. Indeed, real impact will require a change in policy in Asian markets like Vietnam where coal is still a major employer and seen as a driver of economic growth. As a major investor in sovereign debt, even if much of it is in passive funds, BlackRock has enough leverage for meaningful dialogue at least.

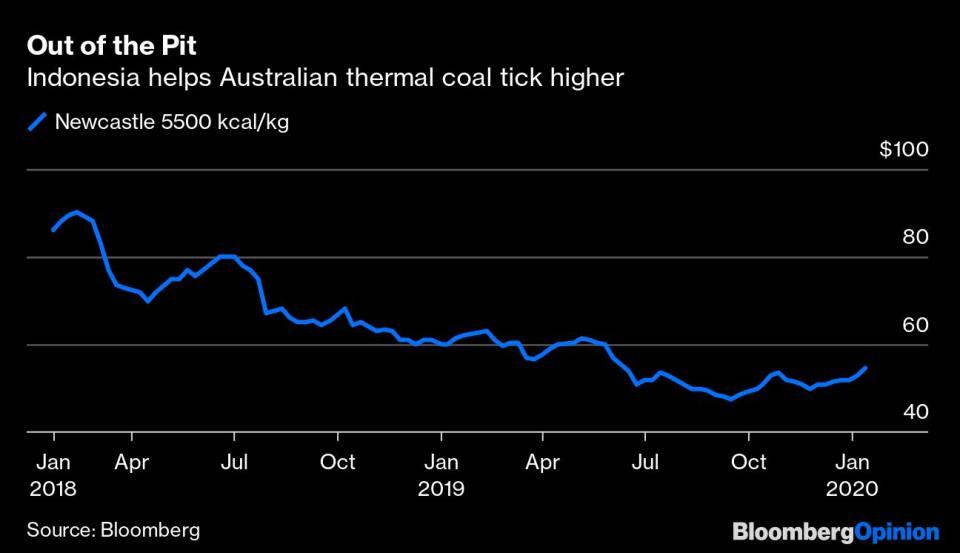

The challenge is significant. Consider China, which wants to reduce its reliance on coal. At least 200 million tons of coal capacity were ready to start production in 2019, while another 409 million tons of government-approved capacity are under construction, according to Bloomberg Intelligence numbers published last September. Together, that’s almost a quarter of China's up-and-running thermal coal capacity. In Indonesia, coal consumption may grow at the world’s fastest pace. Earlier this month, Jakarta ordered coal miners to slash production after record output last year. Prices immediately turned higher.

Policy, then, is the lever to significantly reduce coal use in the region where it’s still growing: Asia. Go back to the UBS numbers. On current trends, the last coal-fired power station closes in six decades. But a red alert scenario where leaders accelerate closures would shutter the last plant in 2058, according to the bank, closer to the 2050 target set by the Intergovernmental Panel on Climate Change.

Indonesia’s tussle with JPMorgan Chase & Co. in 2017 — when Jakarta temporarily severed business ties over a negative research report — is a reminder of just how much emerging market governments care about perception. BlackRock can make that count.

To contact the author of this story: Clara Ferreira Marques at cferreirama@bloomberg.net

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Clara Ferreira Marques is a Bloomberg Opinion columnist covering commodities and environmental, social and governance issues. Previously, she was an associate editor for Reuters Breakingviews, and editor and correspondent for Reuters in Singapore, India, the U.K., Italy and Russia.