Stocks Halt Big Rally Driven by ‘Momentum Guys’: Markets Wrap

(Bloomberg) -- Stocks struggled to make headway, following a furious rally that put the market within a striking distance of its all-time highs.

Most Read from Bloomberg

Sydney Central Train Station Is Now an Architectural Destination

Nazi Bunker’s Leafy Makeover Turns Ugly Past Into Urban Eyecatcher

How the Cortiços of São Paulo Helped Shelter South America’s Largest City

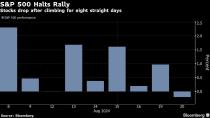

A drop in equities interrupted what would have been the S&P 500’s longest winning streak in 20 years. In stark contrast to the “extreme negative momentum” during the panic selling of early August, “euphoria” has taken hold. In only eight days, the US equity benchmark added almost 8%, with positioning returning to extended levels. Just last week, nearly $16 billion in new long bets were added to S&P 500 futures, according to Citigroup Inc.

In another sign that bullishness has been in overdrive, Bank of America Corp. clients doled out $2.7 billion for US equities during the best week of the year for the S&P 500, with smart money leading inflows. And Goldman Sachs Group Inc. recently said that so-called trend followers were “no longer a headwind” — and were expected to be buyers this week, no matter how markets move.

↵ ↵ ↵

Listen to the Here’s Why podcast on Apple, Spotify or anywhere you listen.

“The momentum guys are driving the bus,” said Kenny Polcari at SlateStone Wealth. “Now the volumes have been trending lower as we move into the end of the month. Moves will be and are exaggerated as a result. And I think the recent rally is proof of that exaggeration.”

At Miller Tabak, Matt Maley said it would be “healthy” if the equity market took a breather for a day or two.

“No market moves in a straight line,” he noted.

Aside from flows and positioning, the recent rally was also fueled by bets the Federal Reserve will signal it’s getting closer to cutting rates. In the countdown to Jerome Powell’s speech Friday in Jackson Hole, Wednesday’s US payrolls revisions are poised to capture Wall Street’s attention.

The S&P 500 fell below 5,600. Nvidia Corp. — which had rallied almost 25% in six days — led losses in megacaps. Bank of America Corp. slumped after Warren Buffett’s Berkshire Hathaway Inc. sold more shares. Lowe’s Cos. cut its full-year guidance. Netflix Inc. hit a record high. Palo Alto Networks Inc. climbed on a bullish outlook and after boosting its buyback program.

Treasury 10-year yields declined six basis points to 3.81%. The loonie trailed most of its major peers as inflation in Canada decelerated, cementing rate-cut wagers. Oil edged lower, with a potential cease-fire in Gaza and mounting concern about the global demand outlook providing bearish headwinds for crude.

Dan Wantrobski at Janney Montgomery Scott, says that he continues to anticipate ongoing stock-market strength on a near-term basis, but he remains on “high alert” for another potentially bigger corrective wave moving through the August-October time frame.

“So what happens when everything and everyone is teed up to be bullish,” Wantrobski said. “From a timing perspective, we are headed into a window where there may be high probability for a liquidity event to occur — and the charts, trader positioning, and sentiment are all very vulnerable right now in our view. We smell a ‘bull trap’ ahead. But hope we’re wrong.”

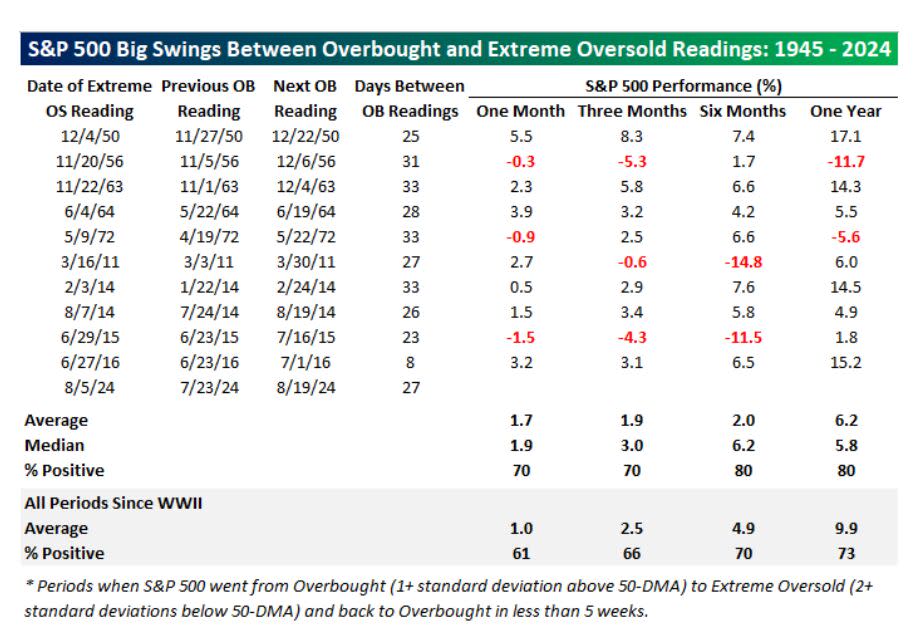

After the S&P 500 last closed at overbought levels on July 23, it quickly sold off and moved into “extreme” oversold territory in just 13 calendar days, according to Bespoke Investment Group. Just as fast as the S&P 500 moved into extreme oversold territory, though, it swung back to overbought levels nearly as fast.

“The market may usually take the stairs up and the elevator down, but in this case, it took the elevator both ways!” the Bespoke strategists said.

Since World War II, there have only been 10 other periods when the S&P 500 moved from oversold levels down to extreme overbought levels and back to overbought levels in less than five weeks.

While the S&P 500’s consistency of positive returns was slightly better than normal, the magnitude of the returns relative to historical averages was mixed, Bespoke noted.

Median one-, three-, and six-month returns were modestly better than the long-term average, but the median one-year gain was well below the post-WWII average.

“While stocks have experienced breathtaking moves in the last month, we would caution against trying to read too much (good or bad) into the swiftness of the rebound,” the strategists concluded.

Momentum traders and a surge in corporate buybacks promise to drive a US stocks rally over the next four weeks, Goldman Sachs Group Inc.’s Scott Rubner said in a note dated Monday.

Rubner, who correctly predicted a late summer correction and advised in late June to trim exposure in US stocks after July 4, has turned tactically bullish saying current positioning and flows “will act as a tailwind as sellers are out of ammo.”

“Strong price momentum and sharp rapid reversals as witnessed over the past month are a feature of modern financial markets, not a bug,” said Jason Draho at UBS Global Wealth Management. “This stems from the outsized market influence of the Fed, macroeconomic uncertainty, investor herd behavior, and the growing use of index-linked products to manage positioning.”

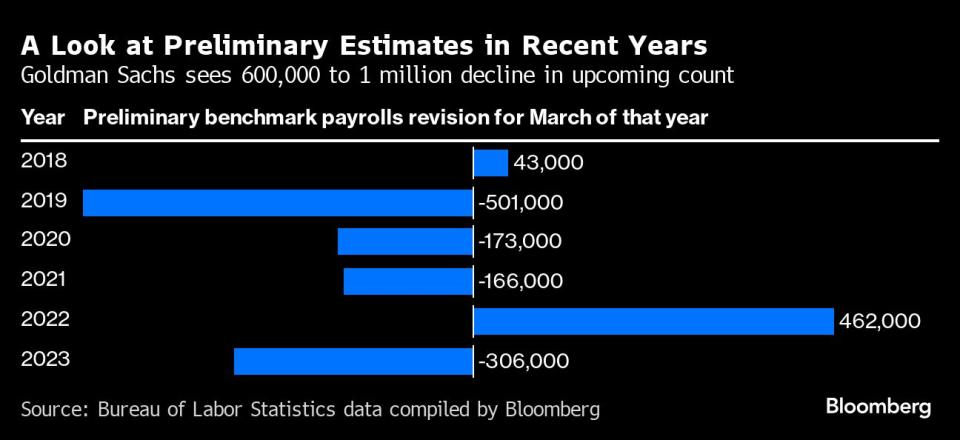

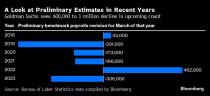

Goldman Sachs Group Inc. and Wells Fargo & Co. economists expect the government’s preliminary benchmark revisions on Wednesday to show payrolls growth in the year through March was at least 600,000 weaker than currently estimated. While JPMorgan Chase & Co. forecasters see a decline of about 360,000, Goldman indicates it could be as large as a million.

“Our guess as to what is driving rates lower today/over the last week is the hyper focus on the payroll revisions,” said Dennis DeBusschere, founder of 22V Research. “People seem to be assuming a large downward revision would increase the odds of more aggressive rate cuts signal at Jackson Hole. That seems fair. Also, it doesn’t mean recession odds go up.”

To Anthony Saglimbene at Ameriprise, continued progress on inflation, moderating but still healthy labor conditions, and economic updates that point to firm consumer trends likely allow the Fed to comfortably begin cutting its policy rate in September.

From a monetary policy perspective, whether it’s a 25 or 50-basis point cut next month isn’t really that important, he noted. What is important — and not lost on investors over the last week or so — is that updates on labor, services activity, inflation, and the consumer all point to a still healthy economic environment, but one that allows the Fed room to start easing monetary policy.

“This is how a soft landing starts, in our view. Of course, there is no guarantee the Fed will ultimately pull it off, but you need the conditions in place to start, and it looks like we finally have those conditions in place today,” he said.

Corporate Highlights:

Microchip Technology Inc. said that its servers were breached by “an unauthorized party,” forcing the chipmaker to shut down some of its systems and scale back operations.

Johnson & Johnson will pay as much $1.7 billion for V-Wave Ltd., bolstering its development efforts to treat heart failure as it goes deeper into medical technology.

Kroger Co. sold $10.5 billion of notes on Tuesday to help fund its acquisition of fellow grocer Albertsons Cos. in one of the biggest corporate bond deals of the year.

Patients taking Eli Lilly & Co.’s blockbuster weight-loss shot were 94% less likely to develop diabetes in a three-year study that illuminates the long-term health benefits of treating obesity.

Alaska Air Group Inc. and Hawaiian Holdings Inc. are one step closer to finalizing their $1.9 billion merger after the US Justice Department decided against challenging it.

Key events this week:

US Fed minutes, BLS preliminary annual payrolls revision, Wednesday

Eurozone HCOB PMI, consumer confidence, Thursday

ECB publishes account of July rate decision, Thursday

US initial jobless claims, existing home sales, S&P Global PMI, Thursday

Japan CPI, Friday

Bank of Japan Governor Kazuo Ueda to attend special session at Japan’s parliament to discuss July 31 rate hike, Friday

US new home sales, Friday

Fed Chair Jerome Powell speaks at Jackson Hole symposium in Wyoming, Friday

Some of the main moves in markets:

Stocks

The S&P 500 fell 0.2% as of 4 p.m. New York time

The Nasdaq 100 fell 0.2%

The Dow Jones Industrial Average fell 0.2%

The MSCI World Index was little changed

Currencies

The Bloomberg Dollar Spot Index fell 0.2%

The euro rose 0.4% to $1.1125

The British pound rose 0.3% to $1.3033

The Japanese yen rose 0.8% to 145.35 per dollar

Cryptocurrencies

Bitcoin rose 0.7% to $59,506.7

Ether fell 0.5% to $2,602.83

Bonds

The yield on 10-year Treasuries declined six basis points to 3.81%

Germany’s 10-year yield declined three basis points to 2.22%

Britain’s 10-year yield was little changed at 3.92%

Commodities

West Texas Intermediate crude fell 0.4% to $74.04 a barrel

Spot gold rose 0.4% to $2,515.22 an ounce

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Isabelle Lee and Vildana Hajric.

Most Read from Bloomberg Businessweek

Losing Your Job Used to Be Shameful. Now It’s a Whole Identity

FOMO Frenzy Fuels Taiwan Home Prices Despite Threat of China Invasion

©2024 Bloomberg L.P.