3 No-Brainer Reasons to Buy Super Micro Computer Before Its Stock Split

Formerly one of the best-performing stocks in the S&P 500 index this year, Super Micro Computer (NASDAQ: SMCI) has been on a wild ride. The stock entered the year around $280, then reached highs of nearly $1,200 in March. After a poor reaction to its fourth-quarter earnings report, the stock is now around $500 per share.

However, it won't stay that way long because management announced a 10-for-1 stock split effective Oct. 1. That will drop the price to around $50 per share (if the valuation stays around its current level). Although it's well off of its high, I think there are still three phenomenal reasons to buy the stock before its stock split.

Supermicro (as it's generally known) has a lot going for it, and it's time for investors to take advantage of the tumble.

Reason No. 1: Supermicro is vital to AI infrastructure

Supermicro makes components and sells full-scale solutions for computing servers. While it has multiple competitors that sell servers, none have the customizability that Supermicro offers. Additionally, Supermicro's servers are some of the most energy-efficient offerings on the market, which is key to long-term sustainability, as these servers consume a lot of power over their lifespan. Supermicro is also a key supplier to many cloud computing giants, which are spending billions of dollars to bulk up their computing power.

Super Micro Computer's market position is incredibly important. It has reaped the benefits of its technologies from increased sales due to the artificial intelligence (AI) race. The AI infrastructure buildout is well under way, but it has a long way to go before peaking.

In fact, the company has raised its long-term revenue goal from $25 billion in annual revenue to $50 billion. Considering that Supermicro's trailing-12-month revenue is just shy of $15 billion, it has a massive runway. Because Supermicro is in its early stages, it looks like a fantastic stock to buy.

Reason No. 2: Fiscal 2025 is projected to be another strong year

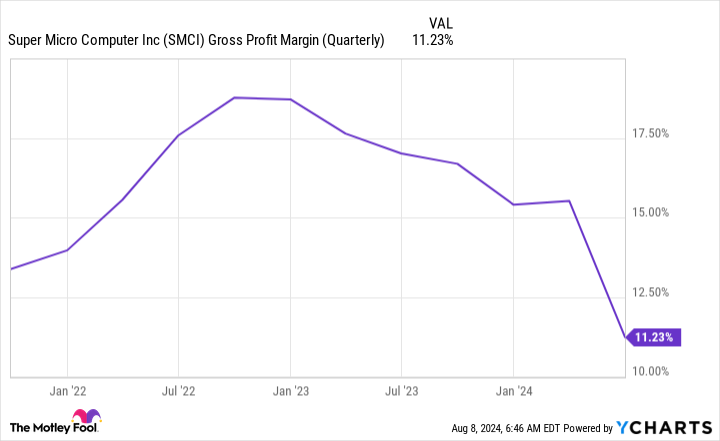

Supermicro recently wrapped up a phenomenal fiscal 2024 (ended June 30) with revenue growth of 143% year over year. However, the company significantly missed earnings per share (EPS) guidance in Q4. At the end of Q3, management expected $7.62 to $8.42 in profits, but the company only delivered $6.25. While this is still strong growth (last year's Q4 saw $3.51 in EPS), a huge miss like this isn't something the market appreciates. The reason for the miss is also concerning: falling gross margins.

This drop was due to "competitive pricing" (otherwise known as cutting its prices to maintain sales) and a higher initial cost to launching its new design specifically related to AI computing clusters. We'll have to see how this shakes out, but management is confident that this is only a temporary headwind.

For fiscal 2025, Supermicro has expected revenue of around $28 billion, indicating around 88% growth. In Q1, that growth is expected to be even higher, coming in at around 207%. That's incredible growth and is a reason to consider buying the stock.

Reason No. 3: The valuation is right

During its peak in March, the stock was incredibly expensive. Now, it's more reasonably priced and looks good moving forward. While management didn't provide any EPS estimates for fiscal 2025, we can use the profit margin posted in Q4 and management's revenue guidance as a guide.

Should Supermicro deliver $28 billion in revenue and maintain the historically low 6.6% profit margin it posted in Q4, it would produce profits of $1.85 billion in 2025. Then, I'll divide its current market capitalization ($28.8 billion) by that projected profit figure to get 15.6 times forward earnings.

That's a great price for a stock, especially considering that the profit margin projection doesn't give Supermicro any credit, as management projects the gross margin pressure to be alleviated by the end of fiscal 2025 and improve steadily throughout the year.

With the bottom end of the valuation projection looking attractive, I think buying Super Micro Computer's stock before the stock split makes good sense, as the company is primed for success over the next few years.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $668,029!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

3 No-Brainer Reasons to Buy Super Micro Computer Before Its Stock Split was originally published by The Motley Fool